Intralinks, in collaboration with the M&A Research Centre at Cass Business School, has produced the first part of a projected two-part report on the last twenty years in the history of the corporate M&A world.

Intralinks, in collaboration with the M&A Research Centre at Cass Business School, has produced the first part of a projected two-part report on the last twenty years in the history of the corporate M&A world.

Part I focuses on “the drivers of shareholder value creation” from M&A activity. Part II, projected for early next year, will look at the M&A strategies “of an elite group of M&A active corporate performers” seeking common attributes and behavior patterns.

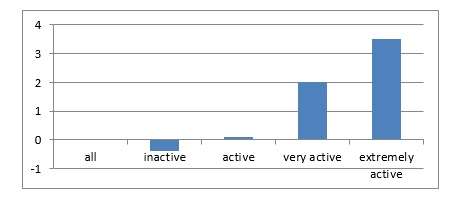

Among the findings of the authors of Part I: “firms outperform the market the more frequently they announce acquisitions.” Quantitatively, they outperform by 0.1% per year during periods when they announce only one or two acquisitions (“active”); by 2% when they announce three to five acquisitions (“very active”); and by 3.5% when they announce six or more acquisitions (“extremely active”.) The only way this can be true, statistically, is if inactive firms underperform the market, because the market as a whole neither under nor over performs itself.

The graph below, adapted from one in the report, may make these numbers vivid.

I ought to insert here the usual and necessary caveat: correlation does not establish causation. But the authors interviewed the chief financial officer of a U.K. based manufacturer of synthetic chemicals, who suggested a causal link. This CFO said, “Companies have to continuously change with the market and experiment and innovate. The fastest way to do this is to buy and sell companies.”

Synchronicity

This report appears almost simultaneous with the resolution of one much-watched M&A drama. The question has been hanging heavy in the air, who will end up owning the maker of Botox and Restasis, Allergan Inc. (NYSE: AGN)? We have an answer: Allergan has found itself a Celtic white knight, Actavis.

Back before Valeant and Pershing Square expressed an interest and put Allergan “in play,” the biopharm target company’s stock price sold for about $120.

Bill Ackman and his corporate alter-ago, Pershing Square, innovated somewhat in the now-closed auction for Allergan, by the closeness with which they allied themselves from the start not merely with the idea that Allergan should sell itself (a common enough position for a corporate activist fund to take) but with a particular bidder, Valeant.

Valeant’s CEO and chairman, J. Michael Pearson, had entered into a confidentiality agreement with Ackman on February 9, and Pershing Square had just two days later formed an entity specifically for use in managing the acquisition, the so-called Co-Bidder Entity PS Fund 1.

As soon as the co-bidders did declare themselves, the target company’s price went to $170. Allergan’s immediate response was resistance. On May 12, the board of the target company announced that the bid “substantially undervalues Allergan, creates significant risks and uncertainties for the shareholders of Allergan, and is not in the best interests of the Company and its shareholders.”

Allergan’s price rose steadily in the months of maneuvering that followed, getting close to $200 even before Actavis swooped in to carry the prize away for $219.

Everyone who “loses” a contest should end up this happy. This amounts to a big win for Ackman, who bought his large stake in Allergan for an average of $126 a share and who will now sell for that $219.

Back to Actavis

Still, though Valeant and Pershing Square make out quite well, Actavis gets the prize. And one can make a strong case that this confirms Intralinks’ point.

This is part of a consistent pattern of acquisitions on the part of Actavis, coming as it does just one and a half years after a merger with Warner Chilcott, and less than a year after the announcement of a merger with Forest Labs, maker of a successful antidepressant – only four months after the completion of that deal.

The whole course of conduct may itself be considered an ongoing experiment into how well various parts mesh, in what creates synergies and what doesn’t, within a dynamic and consolidating industry.