A recent statement by the energy minister of the UAE suggests ‘more of the same.’ Oil prices in early 2015 seem likely to continue the story they were telling in late 2015.

A recent statement by the energy minister of the UAE suggests ‘more of the same.’ Oil prices in early 2015 seem likely to continue the story they were telling in late 2015.

On Tuesday, January 13, the minister, Suhail bin Mohammed al-Mazrouei said that the Organization of the Petroleum Exporting Countries isn’t going to shore up “a certain price” by cutting production.

Crude oil slides on and on and is now (mid-January 2015) below $50 a barrel. The broader investment consequences of this, both the obvious and the obscure, continue to unfold.

Reading it Right

Nothing much turns (for the pursuit of alpha anyway) on the unfolding of the obvious consequences. The markets simply discount them. But a lot depends on reading right the more obscure consequences. All we have thus far are the earliest reports from that effort.

On a somewhat-related note: hedge funds ended 2014 in positive territory, according to figures compiled by the independent data provider Eurekahedge.

Funds were up 4.57% for the year: though that’s hardly cause for celebration, since the MSCI World Index returned 6.79% over the same year.

Another way of measuring the rather uninspiring performance of the year is this: although in 2013 35% of hedge fund managers posted double-digit returns, in 2014 only 18% did so.

Yet another Eurekahedge metric: the growth of asset base. The U.S. hedge fund industry expanded its base in 2014, but only at half the rate it did in 2013 (an increase of $240.4 billion in 2013, an increase of $125.9 billion in 2014).

By Region

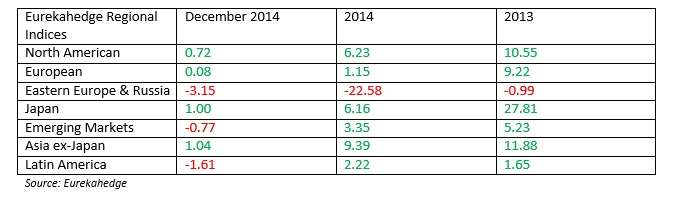

Performance varied widely among regions, as the table below indicates.

Source: Eurekahedge

In December, and for the year 2014 as a whole, the best performing region was Asia ex-Japan.

The Goliath of that region, China, is as Eurekahedge puts it just now “treading the path of moderation, with annual GDP growth rate hovering around 7% which adds to the overall concern regarding global economic growth.” The China CSI 300 index rose 25.81% during December. Interest rate cuts of the previous months had sparked a “raging bull market” as Eurekahedge observes, and this has combined with improved property markets and “improved investor access from the Shanghai-Hong Kong stock connect.”

But to return to oil: China has been a net importer since 1993. Unmentioned by Eurekahedge, but pertinent: in December 2014 its oil importation rate rose above 7 million barrels a day. As the Financial Times has recently observed, current conditions present “an unusual opportunity for China to increase reserves” at bargain cost.

Japan too is heavily dependent on imported oil, although other matters still seem to be on the minds of its policy makers.

On the other side of the import/export statistics, national economies that depend on the export of oil had a tough time in 2014: Russia notably.

Terrible Memories

For hedge funds with mandates for Eastern Europe and Russia, December was the sixth consecutive month of losses. The good news, such as it is, is that such hedge funds outperformed the Russian RTS stock market, which was down 18.84% in December.

As the year ended, Russia’s central bank engaged in drastic measures to protect the rouble. The measures included the biggest interest rate rise (to 17%) since 1998. The year 1998 itself is not a time blessed in the memory of outside investors who had interests in Russia at the time.

Even more important, and as Shane Brett has cautioned here in recent days, “A collapsing Russia will be very dangerous for the rest of the world.”

One Play

Looking at strategic indices, Eurekahedge observes that CTA-managed futures won the best-in-show award for December, largely on the strength of reading energy right, “with short energy positions once again dominating performance…” and that currencies also assisted the CTA victory, with an extended rally in the U.S. dollar.

Going forward, one way to play the consequences of the continuing drop in crude oil prices may be by betting on the junk bond default rate. Eurekahedge is not giving out advice, but it does say, “A number of energy producing companies … borrowed heavily in the high yield markets to finance their operations” of late. With decreasing prices these companies will have great difficulty servicing that debt.