What struck me while interviewing Brian Shapiro about the current state of the hedge fund world’s MBS space was his enthusiasm about Structured Portfolio Management, an MBS focused firm based in Stamford, CT and run by Don Brownstein.

What struck me while interviewing Brian Shapiro about the current state of the hedge fund world’s MBS space was his enthusiasm about Structured Portfolio Management, an MBS focused firm based in Stamford, CT and run by Don Brownstein.

I mentioned that outside of agency-backed MBS, the market for mortgage securitizations by private financial institutions essentially disappeared during the global financial crisis 2007-08 and then made something of a comeback by 2010.

That is true, he said, but “there has been a downslope” over the last 18 to 20 months, and there is now a “high level of correlation,” which indicates investors should be wary. Not that they should stay away but that they should “go with managers with tenure and track record in the sector.” Distressed plays and Asia remain areas of interest in the MBS fund worlds.

“Agency was a two-year pop until it flickered out.” Nor can one really expect that agency will come back so long as the economy is good.

I’ll get back to that later, and I’ll decode the graph you see here. But for now … SPM.

SPM “sticks out in [his] mind” as a successful manager with a “17 year track record” with returns in the mid 20s. “Where else are you going to go to get that?” Well, there is at least one other place that then came to Shapiro’s thoughts: SPM’s return compares to the return available from Elliott.

But with a multi-strategy fund like Elliott, there’s less of a sense of what you’re buying into. “You’re going after Argentina one week, Hess Corp. the next. The gamma on a big multi-strat book helps make the case for Brownstein.”

For those who might benefit from a refresher course:

- Gamma is the rate of change of delta;

- Delta is the change in the price of the underlying asset that corresponds to a given change in the price of a derivative, that is, the hedge ratio;

- All else being equal, an investor presumably wants to keep the hedge ratio stable, that is, to keep gamma low;

- Elliott’s ongoing efforts to enforce its judgment against Argentina is the stuff of legend;

- Hess Corp. entered into a last-minute settlement of a fierce proxy contest with Elliott in May 2013.

At any rate, the point is that Brownstein has helped demonstrate the valuable role that MBS oriented hedge funds can play in the portfolio of many investors. In comparing him to Paul Singer, Shapiro is putting the best of one class up against the best of another.

RMBS/CMBS Hedge Fund Peer Report

These points arise because Shapiro is the President and managing member of Simplify LLC, an investment-management consultant. Simplify has just released its 2014 Year End RMBS/CMBS Hedge Fund Peer Report.

I asked whether and to whom the report was worth $2,500.

“It is worth it to anyone looking to allocate to or to reduce their allocation to this space.”

As to audience, the report is directed at any qualified investor or their intermediary.

“Worth is subjective. We’re confident that this report compares favorably in information and completeness to anything you’re purchasing right now,” he said.

Will this be an annual event (the release of the report). No, Shapiro told me, Simplify is working on quarterly updates. –

He founded the company two years ago out of the conviction, he says, “there’s got to be a better way for investors to find portfolio managers” who meet their needs, than anything yet in the marketplace. Simplify is devoted to “curating people into effective peer groups, and not just dumping a lot of data on the world and saying, ‘go fish.’”

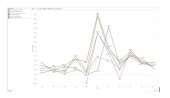

Some Decoding

The above graph is the picture of a bubble (broken down into components, a fact that rather strains the metaphor of a bubble!). Or of a bubble and its aftermath. Still, the lines show peer-group returns for various sorts of mortgage-bond oriented fund beginning in 2004. Though the lines of course aren’t perfectly correlated, five out of the six of them come to a peak and head down at 2009, four of those quite sharply so.

Those four are: red (residential agency peer index); green (agency and non-agency peer index); brown (residential and commercial real estate diversified peer index); and purple (residential non agency peer index). The one that heads downward somewhat less sharply than its peers at that moment is the yellow line, representing distressed mortgages. The one that peaks a little later than the others is the blue line, the commercial mortgages peer index.

The correlation among these lines tightens up as one glances toward the right side of the page. All the lines rise promisingly in 2012, and they all drop off sin 2013. The only one that rises slightly in 2014 is green.