By Jason Hill, SVP and David O’Donohue, VP, Calamos Investments

When it comes to your investment portfolio, volatility can be an unsettling word. For strategies that utilize convertible arbitrage though, market volatility can be a welcomed phenomenon, as we may be able to profit from it through what is referred to as gamma trading. In a convertible arbitrage strategy, we are buying convertible bonds and selling short shares of the underlying stock as a hedge. If the stock rises, we will lose money on the shares we are short but we will make money on the bonds we own as they appreciate in value.

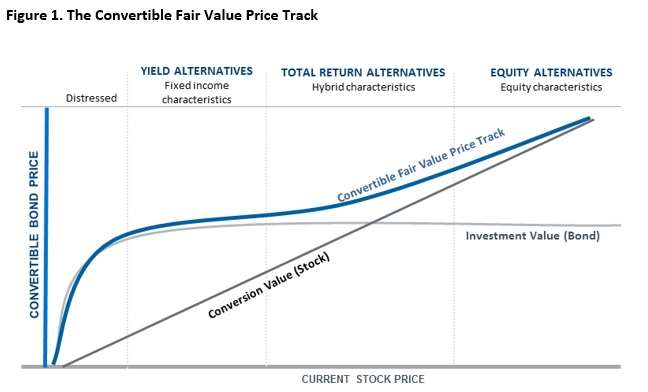

This brings us to our topic, gamma trading. To understand gamma trading, we have to begin with another Greek letter: delta. Keep in mind that from here on out, we’ll be discussing theoretical outcomes, not the performance of any security. If you look at the convertible fair value price track (Figure 1), you can see that as the price of the underlying stock rises, the convertible value rises, and as the stock value falls, the convertible value falls as well. (For more on the convertible fair value price track, see the Calamos guide.) How much the convertible value rises or falls for a given stock move is referred to as delta. The higher the delta, the higher the sensitivity to the stock’s moves.

If we look back at the price track, we can see that sensitivity to stock moves (delta) increases as the stock price advances and the bond becomes more equity-like (higher delta). Price sensitivity falls as the stock price declines and the convertible becomes more bond-like (lower delta). The change in delta as stock price moves is what we refer to as gamma.

Now the big question: how might we profit from this?

As noted earlier, in a convertible arbitrage strategy, if a stock rises, we will lose money on the shares we are short but we will make money on the bonds we own as they will appreciate in value. If we think the stock is undervalued, we can short fewer shares (a bullish hedge). Or, if we think a stock is overvalued, we can short more shares (a bearish hedge). More frequently however, we implement what is called a delta neutral hedge. If we are on a delta neutral hedge, the money we make on the bond and the money we lose on the stock should be equal and offset. Unlike a bullish or bearish hedge where we are seeking to profit from the stock rising or falling, a delta neutral hedge seeks to profit simply from stock volatility.

As we discussed earlier, as the stock moves, our delta changes (gamma) and we need to adjust our position if we wish to maintain a similar hedge. As the stock rises, our delta increases, which means we need to short additional shares to stay on a similar neutral hedge. Conversely, as the stock falls, our delta falls and we need to cover shares to remain on the neutral hedge. From a mechanical standpoint, we continually sell as a stock advances (sell high) and buy as a stock declines (buy low). The more volatility in the market, the more stocks rise and fall—which can give us more opportunities to sell high and buy low.

Let’s look at a hypothetical example. We own an XYZ convertible bond that converts into 100 shares of XYZ stock and has a .50 delta. On Day 1, we would short 50 shares of XYZ stock to be on a neutral hedge. If on Day 2 the stock rises and our delta increases to .60 we would short another 10 shares of stock to remain neutral. Let’s say on Day 3 or Day 4 the stock price declines back down to the original Day 1 level. We would then buy back the extra 10 shares we shorted. We would still be on a neutral hedge with the same bond and stock prices as on Day 1 but we now have real profits booked on shares we sold high and then bought low.

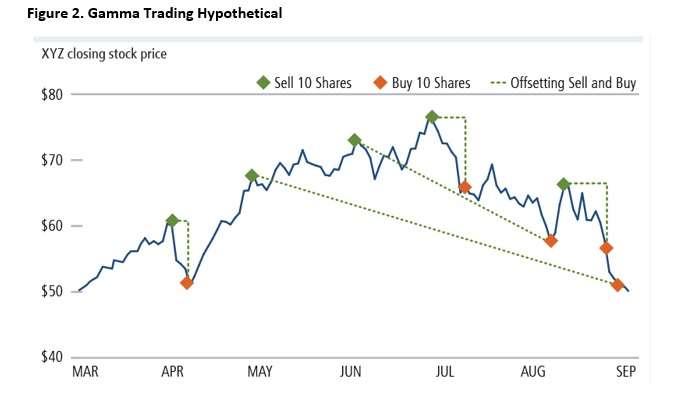

In Figure 2, we show an example of gamma trading over a longer period. The chart shows five sales and five purchases of XYZ, which together produce the desired pattern of buying low and selling high. As the stock price moves, we buy or sell based on the change in delta (gamma). At the end of the period, the stock price is very similar to where it was at the start of the period, and theoretically, the convertible bond price and the delta would be fairly similar to their starting levels, as well. If we had simply held the position, we may have only minimal profits or losses. However, in this hypothetical example, we have locked in realized profits from the five sets of gamma trades.

The above example is not meant to represent the performance of any given security. It is a hypothetical illustration of general investment themes.

So while big market swings may not be comfortable for most investors, they can provide a convertible arbitrage strategy with lots of gamma trading opportunities.

Alternative investing strategies, such as gamma trading, are not appropriate for all investors. The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors also may have an effect on the convertible security’s investment value.

Convertible Arbitrage Principal Risks: Convertible Securities Risk- The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increasing as interest rates decline. The credit standing of the issuer and other factors also may have an effect on the convertible security’s investment value. Convertible Hedging Risk- If the market price of the underlying common stock increases above the conversion price on a convertible security, the price of the convertible security will increase. The portfolio’s increased liability on any outstanding short position would, in whole or in part, reduce this gain.

Short Sale Risk: A portfolio may incur a loss (without limit) as a result of a short sale if the market value of the borrowed security increases between the date of the short sale and the date the portfolio replaces the security. The portfolio may be unable to repurchase the borrowed security at a particular time or at an acceptable price.

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Information contained herein is for informational purposes only and should not be considered investment advice.