By Scott Opsal Relative Performance Actively managed funds have recently underperformed passive indexes. As a result, fund inflows and deposits have favored passive funds. Active Vs. Passive Return Patterns Are Cyclical Our research suggests relative returns between active and passive are cyclical, depending on the market environment. We examine several factors that may explain this pattern and shed light on current trends. Today’s Conditions Tilt Toward Passive Today’s conditions are optimal for passive results. Investors should keep this in mind and avoid concentrating their assets in passive vehicles, as performance chasing rarely works out well. A mixed approach seems to be the more enlightened strategy. Passive Leadership Not Perpetual Weather is one of the many challenges that make golf a fascinating and frustrating game. Calm days are a delight and scoring conditions are at their very best. A light breeze can be refreshing and adds a bit of thrill to the shot, requiring small changes in club selection. A stronger wind requires a two-club allowance and becomes a significant impediment to scoring, requiring major adjustments to the shot. Gusts over 20 mph create a three-club headwind and good scores become nearly impossible. The ball flight rarely matches what is intended and the player must select much longer clubs to fight the wind. Heavy winds present a nearly insurmountable hurdle for weekend duffers, whose main hope is that their hats don’t blow into the pond and their umbrellas don’t turn inside out, and who soon find themselves wondering why they had not picked a more sensible indoor pastime like cribbage. Many active managers today will recognize a familiarity to that last sentence. Recent returns show that few active managers are outperforming passive index funds in the current market environment, and investors are wondering whether this is a permanent state of affairs (spoiler alert: it isn’t!). A client inquiry led us to look into one particular aspect of this discussion we’ve often thought about but never closely examined. Ever since the first index fund was launched in 1975, investors have been debating the merits of active versus passive portfolio management with considerable zeal. The discussion is multi-faceted; practical and philosophical. Some of the topics that enter into the debate are…

- Do some active managers have skill that adds value to the investment process?

— Undoubtedly.

- Can investors identify the benchmark index that best matches their objectives and constraints? — Less often than you think.

- Are most investors able to define and measure the amount of true investment risk taken? — In my opinion, no.

- Do performance studies properly incorporate a cost-benefit analysis of the advice, counseling, education, hand-holding and safeguards against behavioral errors that investors receive from their active managers and advisors? — I haven’t seen one yet.

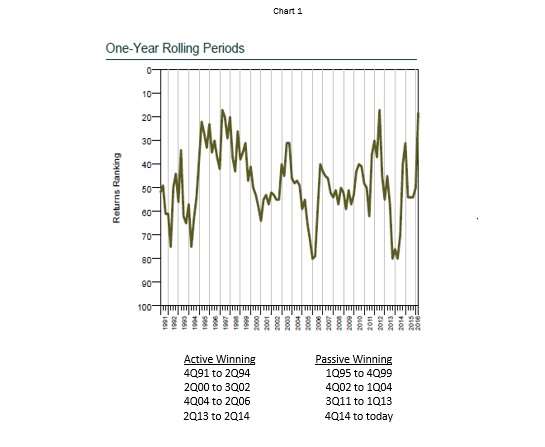

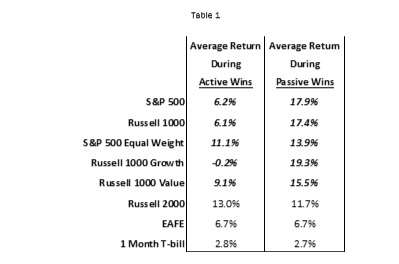

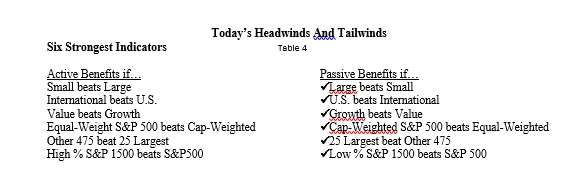

Active Vs. Passive Cyclicality Tackling all of these topics in one memo would be unwieldy. Our objective is to examine a particular aspect of the discussion that can be analyzed quantitatively, namely the cyclicality of the relative performance of active versus passive management. Index funds do not always beat active funds, nor do stock pickers always outperform the index. There is a to-and-fro between management styles; one style wins for a time and then the other takes the lead. (Cyclicality and reversals of fortune seem to pop up everywhere in our profession!) As we shall find, the best management style isn’t either/or, but rather, both. Chart 1 from Callan Associates illustrates the rolling nature of this ebb and flow. The chart shows the percentage of Callan’s active Large Cap domestic managers outperforming the S&P 500 over the previous twelve months (gross). When the rolling performance line is above 50%, the index is beating most active managers; when it’s below 50%, most active managers are outperforming the index. This graph along with our own experience tell us that relative returns between active and passive vary over time. There are times when the battle is a draw, while in other periods the advantage lies with one or the other. Looking back to 1991, we identified four windows of time in which active performed best, and four other periods when passive had the upper hand (the count of four each is coincidental).  This study is designed to examine our hypothesis that the relative performance of active versus passive strategies is cyclical in nature, and that it may be possible to identify the market conditions and manager habits accounting for that cyclicality. Based on many years in the institutional investment business and our interactions with hundreds of active and passive managers, we identified nine test factors we felt might explain active/passive return cycles. These return drivers are grouped into three categories to aid in our analysis, and we provide our rationale why each factor might help explain active/passive cyclicality. The first grouping is referred to Index Mismatch because it represents asset classes outside the U.S. Large Cap index that are often found in active managers’ portfolios. The second group is labeled Market Internals: Valuation; the third is Market Internals: Size. These factors address differences within the U.S. Large Cap equity space rather than comparisons across different asset classes. In each case, we structured the factor to have a positive reading under conditions we believed would benefit active managers, and a negative value when we felt the factor would hurt active managers. Index Mismatch Factors 1) Small Cap minus Large Cap (S&P 500 minus Russell 2000): This factor accounts for the fact that many active managers hold smaller companies outside the S&P 500. As structured, this factor will produce a positive value when Small Caps outperform (benefiting active managers owning Small Caps) and will read negative when Large Caps outperform, making the active managers’ smaller holdings a performance drag. 2) International minus U.S. (EAFE minus S&P 500): As with Small Caps, active managers may go “off the board” and own international companies not included in the S&P 500. If international stocks are winning, this tilt should be an advantage; if international returns lag these holdings should be a headwind. 3) Cash minus S&P 500: Active managers hold cash for administrative and strategic reasons and will underperform whenever stocks outperform cash and, at today’s rates, they’ll only win by holding cash when equity markets fall. Market Internals: Valuation The first sub-group under Market Internals deals with the topic of valuation. Our experience suggests that most active managers pay some attention to valuation and may tend to eschew extremely high multiple stocks and companies losing money. 4) Value minus Growth (Russell 1000 Value minus Russell 1000 Growth): One test of valuation sensitivity is simply to model in a Value bias using the Russell 1000 style indices, with the thought that market conditions favoring Value will also favor active, while Growth markets tend to benefit passive portfolios. (We utilized Russell indexes due to the longer performance history.) 5) “The Rest” minus High P/E; and 6) “The Rest” minus Negative Earnings: We extended the concept behind factor #4 by splitting the S&P 500 into three groups: (a) stocks with P/E ratios above 40; (b) stocks currently losing money (negative P/E ratios); and, (c) “the rest” which holds profitable companies with P/E ratios under 40. This plays to our belief that a meaningful number of active managers have a hard time paying more than 40 times for a stock and tend to fish in “the rest” of the pond. Likewise, we believe many active managers have a tendency to avoid or ignore companies that are currently losing money. Under our hypothesized model, when “the rest” win we expect it will benefit active managers. If the profitable and reasonably priced “rest” of the market is outperforming, we expect the index to suffer because it doesn’t have a predisposition to avoid stocks in either tail. When the over-40 P/E and/or money-losing companies are outperforming we expect the valuation-insensitive index to come out ahead. Market Internals: Size The second sub-group under Market Internals deals with market cap. Our hypothesis is that indexes outperform when the very largest stocks outperform. Indexes can become top heavy when glamour stocks run up, whereas active managers may underweight the largest companies as a matter of portfolio construction or valuation. 7) Equally-Weighted S&P 500 minus Cap-Weighted S&P 500: S&P publishes an equally- weighted version of its traditional cap-weighted 500 index. By giving each company equal weight, this version reduces the impact Mega-Caps have on returns and reflects the performance of all 500 companies on a broad and equal basis. Our hypothesis is that when the equally-weighted S&P 500 is outperforming, active managers will benefit. When the top- heavy traditional S&P 500 is winning, index funds should have an advantage. 8) Percent of the S&P 1500 beating the S&P 500: This is the first of two indicators we constructed to expand on this notion. We count how many stocks in the S&P 1500 (Large, Mid and Small Caps) are beating the overall S&P 500 return. When this ratio is high, the average company is doing well which should give active managers a tailwind. When this ratio is low, Mega-Caps are in control and passive funds may benefit in such a concentrated environment. 9) “The Rest” minus Largest 25: Our last custom factor divides the S&P 500 into two buckets: the 25 largest companies and all “the rest.” When “the rest” perform well, active managers should prosper, and when the largest 25 do well we should see passive coming out stronger. Calculations We calculated the quarterly spread between each of these factor pairs going back to 1991 when possible. The resulting values show the performance of the first member of the pair (the active-manager-friendly term) minus the second member of the pair (the passive-friendly term). Each factor return is then shown on a trailing 12-month window to correspond with Chart 1. The goal of these return calculations is to test our hypothesis that the active/passive return cycle can be attributed to certain market environments which occasionally favor one style or the other. Table 1 shows the average trailing 12-month return for various asset classes used in this study, sorted according to the active/passive relative performance cycle. We identified 33 quarters since 1991 where active managers appeared to have the clear advantage over the index (labeled “active wins”). There were 39 quarters where the index had a clear advantage — dominated by a 20-quarter run during the tech bubble (labeled “passive wins”). The remaining windows of time, in which roughly half the active managers outperformed and half underperformed, are excluded as neutral periods for this analysis. Table 1 tells a compelling story even before we get to the core of our research. Those windows of time in which active management won saw the S&P 500 earn an average +6.2% annualized return, while periods in which the index prevailed had an average S&P 500 return of +17.9%, a dramatic contrast. The three Large Cap Russell indices show the same strong indication of weaker returns favoring active, and stronger returns favoring passive. Periods of modest returns do not thrill investors but they clearly favor active management styles. We were surprised to find that Small Cap and international stocks did not show a similar bias. Both of these asset classes produced roughly equivalent returns when either active management or passive won. This is one of the more curious results and needs to be considered as we examine the rest of our data.

This study is designed to examine our hypothesis that the relative performance of active versus passive strategies is cyclical in nature, and that it may be possible to identify the market conditions and manager habits accounting for that cyclicality. Based on many years in the institutional investment business and our interactions with hundreds of active and passive managers, we identified nine test factors we felt might explain active/passive return cycles. These return drivers are grouped into three categories to aid in our analysis, and we provide our rationale why each factor might help explain active/passive cyclicality. The first grouping is referred to Index Mismatch because it represents asset classes outside the U.S. Large Cap index that are often found in active managers’ portfolios. The second group is labeled Market Internals: Valuation; the third is Market Internals: Size. These factors address differences within the U.S. Large Cap equity space rather than comparisons across different asset classes. In each case, we structured the factor to have a positive reading under conditions we believed would benefit active managers, and a negative value when we felt the factor would hurt active managers. Index Mismatch Factors 1) Small Cap minus Large Cap (S&P 500 minus Russell 2000): This factor accounts for the fact that many active managers hold smaller companies outside the S&P 500. As structured, this factor will produce a positive value when Small Caps outperform (benefiting active managers owning Small Caps) and will read negative when Large Caps outperform, making the active managers’ smaller holdings a performance drag. 2) International minus U.S. (EAFE minus S&P 500): As with Small Caps, active managers may go “off the board” and own international companies not included in the S&P 500. If international stocks are winning, this tilt should be an advantage; if international returns lag these holdings should be a headwind. 3) Cash minus S&P 500: Active managers hold cash for administrative and strategic reasons and will underperform whenever stocks outperform cash and, at today’s rates, they’ll only win by holding cash when equity markets fall. Market Internals: Valuation The first sub-group under Market Internals deals with the topic of valuation. Our experience suggests that most active managers pay some attention to valuation and may tend to eschew extremely high multiple stocks and companies losing money. 4) Value minus Growth (Russell 1000 Value minus Russell 1000 Growth): One test of valuation sensitivity is simply to model in a Value bias using the Russell 1000 style indices, with the thought that market conditions favoring Value will also favor active, while Growth markets tend to benefit passive portfolios. (We utilized Russell indexes due to the longer performance history.) 5) “The Rest” minus High P/E; and 6) “The Rest” minus Negative Earnings: We extended the concept behind factor #4 by splitting the S&P 500 into three groups: (a) stocks with P/E ratios above 40; (b) stocks currently losing money (negative P/E ratios); and, (c) “the rest” which holds profitable companies with P/E ratios under 40. This plays to our belief that a meaningful number of active managers have a hard time paying more than 40 times for a stock and tend to fish in “the rest” of the pond. Likewise, we believe many active managers have a tendency to avoid or ignore companies that are currently losing money. Under our hypothesized model, when “the rest” win we expect it will benefit active managers. If the profitable and reasonably priced “rest” of the market is outperforming, we expect the index to suffer because it doesn’t have a predisposition to avoid stocks in either tail. When the over-40 P/E and/or money-losing companies are outperforming we expect the valuation-insensitive index to come out ahead. Market Internals: Size The second sub-group under Market Internals deals with market cap. Our hypothesis is that indexes outperform when the very largest stocks outperform. Indexes can become top heavy when glamour stocks run up, whereas active managers may underweight the largest companies as a matter of portfolio construction or valuation. 7) Equally-Weighted S&P 500 minus Cap-Weighted S&P 500: S&P publishes an equally- weighted version of its traditional cap-weighted 500 index. By giving each company equal weight, this version reduces the impact Mega-Caps have on returns and reflects the performance of all 500 companies on a broad and equal basis. Our hypothesis is that when the equally-weighted S&P 500 is outperforming, active managers will benefit. When the top- heavy traditional S&P 500 is winning, index funds should have an advantage. 8) Percent of the S&P 1500 beating the S&P 500: This is the first of two indicators we constructed to expand on this notion. We count how many stocks in the S&P 1500 (Large, Mid and Small Caps) are beating the overall S&P 500 return. When this ratio is high, the average company is doing well which should give active managers a tailwind. When this ratio is low, Mega-Caps are in control and passive funds may benefit in such a concentrated environment. 9) “The Rest” minus Largest 25: Our last custom factor divides the S&P 500 into two buckets: the 25 largest companies and all “the rest.” When “the rest” perform well, active managers should prosper, and when the largest 25 do well we should see passive coming out stronger. Calculations We calculated the quarterly spread between each of these factor pairs going back to 1991 when possible. The resulting values show the performance of the first member of the pair (the active-manager-friendly term) minus the second member of the pair (the passive-friendly term). Each factor return is then shown on a trailing 12-month window to correspond with Chart 1. The goal of these return calculations is to test our hypothesis that the active/passive return cycle can be attributed to certain market environments which occasionally favor one style or the other. Table 1 shows the average trailing 12-month return for various asset classes used in this study, sorted according to the active/passive relative performance cycle. We identified 33 quarters since 1991 where active managers appeared to have the clear advantage over the index (labeled “active wins”). There were 39 quarters where the index had a clear advantage — dominated by a 20-quarter run during the tech bubble (labeled “passive wins”). The remaining windows of time, in which roughly half the active managers outperformed and half underperformed, are excluded as neutral periods for this analysis. Table 1 tells a compelling story even before we get to the core of our research. Those windows of time in which active management won saw the S&P 500 earn an average +6.2% annualized return, while periods in which the index prevailed had an average S&P 500 return of +17.9%, a dramatic contrast. The three Large Cap Russell indices show the same strong indication of weaker returns favoring active, and stronger returns favoring passive. Periods of modest returns do not thrill investors but they clearly favor active management styles. We were surprised to find that Small Cap and international stocks did not show a similar bias. Both of these asset classes produced roughly equivalent returns when either active management or passive won. This is one of the more curious results and needs to be considered as we examine the rest of our data.  Identifying Headwinds And Tailwinds During each window of time, we calculated the return spreads for the factors and tallied whether or not the sign was correct, given our hypothesized model. For example, if Small Cap strength should benefit active managers, we tallied a yes if Small Cap actually did outperform during periods of active outperformance, and we tallied a no if Small Caps underperformed even though active was winning. This tally gives us a hit rate for each factor which measures how often the factor results confirmed our proposed explanations. Let’s examine the results of our analysis using the Small Cap minus Large Cap factor as an example. The periods clearly identified as either active dominant or passive dominant represent our control variable; we then mapped each return driver against those periods. For example, we expect active managers to win when Small Caps are stronger, and passive to win when Large Caps are outperforming. Table 2 shows the average 12-month return spread for Small Cap minus Large Cap was a minimal +0.3% over the entire study. However, in periods when active managers were outperforming, the Small Cap minus Large Cap spread was +6.8%, while in periods when passive was winning the spread was -6.2%. The table also shows that Small Cap minus Large Cap had an excellent hit rate, registering the “correct” sign in 82% of active win quarters and in 77% of passive win quarters. Spread and hit rate both seem to confirm a link between Small Cap outperformance and active management wins.

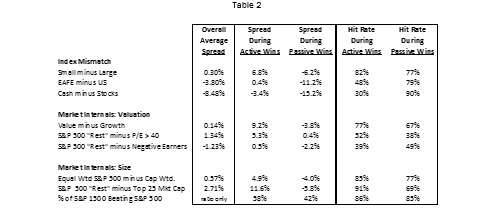

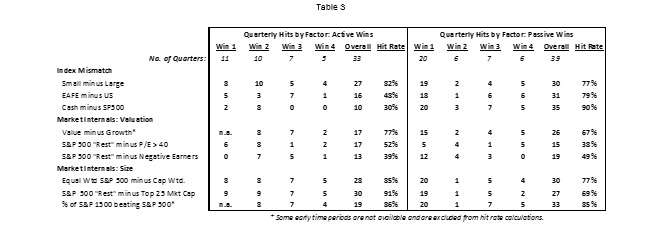

Identifying Headwinds And Tailwinds During each window of time, we calculated the return spreads for the factors and tallied whether or not the sign was correct, given our hypothesized model. For example, if Small Cap strength should benefit active managers, we tallied a yes if Small Cap actually did outperform during periods of active outperformance, and we tallied a no if Small Caps underperformed even though active was winning. This tally gives us a hit rate for each factor which measures how often the factor results confirmed our proposed explanations. Let’s examine the results of our analysis using the Small Cap minus Large Cap factor as an example. The periods clearly identified as either active dominant or passive dominant represent our control variable; we then mapped each return driver against those periods. For example, we expect active managers to win when Small Caps are stronger, and passive to win when Large Caps are outperforming. Table 2 shows the average 12-month return spread for Small Cap minus Large Cap was a minimal +0.3% over the entire study. However, in periods when active managers were outperforming, the Small Cap minus Large Cap spread was +6.8%, while in periods when passive was winning the spread was -6.2%. The table also shows that Small Cap minus Large Cap had an excellent hit rate, registering the “correct” sign in 82% of active win quarters and in 77% of passive win quarters. Spread and hit rate both seem to confirm a link between Small Cap outperformance and active management wins.  EAFE minus U.S. appears, on the surface, to support our hypothesis with a 79% hit rate during passive win periods, and a clear return gap of +0.4% during active wins compared to -11.2% during passive wins. A deeper look calls this into question. Table 1 contains the average 12-month returns by asset class during the active win and passive win periods (note Table 1 shows absolute returns not spreads.) We find that EAFE itself experienced the same return during active and passive winning timeframes. This means that the spreads and hits we see in Table 2 are not due to differences in international stock returns but rather are driven by the differences in U.S. stock returns. Also note that the overall EAFE minus U.S. spread was -3.8% over the entire study, the worst of the lot outside of cash. We believe this accounts for the 48% hit rate during active wins; EAFE was such a laggard that its ability to support active managers was tepid at best. The fact that EAFE returns are the same for both active and passive winning timeframes leads us to conclude that the returns of foreign stocks on their own are not a key driver of the active/passive cycle. Cash is the third Index Mismatch asset class. Since equity markets tend to rise over time, cash is a nearly constant drag on active performance. We bring nothing new to the table when we note that cash hurts active managers the most in strong up markets, and near-zero rates today require absolute losses in equities for cash to help at all. Shifting to our analysis of Market Internals, we find a strong storyline develops for some of these factors while others fail to give compelling signals. Value minus Growth has a near-zero average spread over the entire study, but Value trumps Growth by +9.2% when active wins and lags by -3.8% when the index wins. The hit rate is 77% during active wins and 67% during passive wins. The relative spread of Value over Growth is clearly related to active manager wins, and Growth’s recent supremacy is one reason why indexing has been on such a run of late. Our two customized valuation measures fail to deliver strong signals. The Rest minus High P/E had a +1.34% spread over the study and returns are more favorable during active wins. However, the hit rate is no better than random and does not give us much confidence in this indicator. The Rest minus Negative Earners displays a -1.23% spread (silly us, thinking that profitability matters) but the hit rate again fails to inspire confidence. Our first size-focused metric is the Equal-Weighted S&P 500 versus Cap-Weighted S&P 500. Equal weighting has a +0.57% spread overall and outperforms by an average of +4.9% during active manager wins, while it lagged by -4.0% during passive wins. The hit rates of 85% and 77% are among the highest in our study. The Rest minus 25 largest S&P 500 is also very robust. This metric has the highest positive spread over the entire study at +2.71%, meaning that, on average, the 25 largest S&P holdings have underperformed the other 475 over time. The window-specific results are also extremely encouraging with an +11.6% spread during active wins and a -5.8% spread during passive wins, along with very high hit ratios in both columns. Our final size-based factor is the percent of S&P 1500 stocks beating the S&P 500. Return spread is not calculated as this is a ratio-formatted variable, but as we examine the count of S&P 1500 winners we again see encouraging hit rates in both environments. Table 3 shows the granular data on hit rates for each of the eight discrete periods in our analysis. Small Cap minus Large Cap appears robust in seven of the eight periods, with the second passive win timeframe a notable exception (more on this event later).

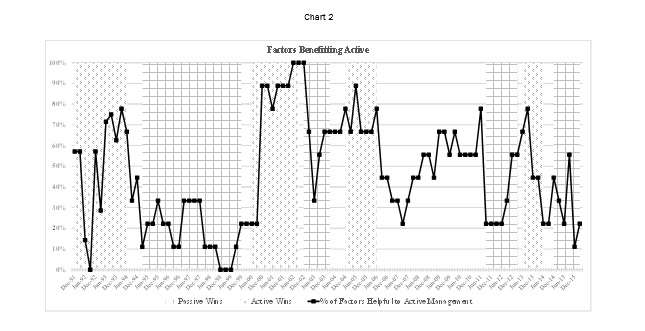

EAFE minus U.S. appears, on the surface, to support our hypothesis with a 79% hit rate during passive win periods, and a clear return gap of +0.4% during active wins compared to -11.2% during passive wins. A deeper look calls this into question. Table 1 contains the average 12-month returns by asset class during the active win and passive win periods (note Table 1 shows absolute returns not spreads.) We find that EAFE itself experienced the same return during active and passive winning timeframes. This means that the spreads and hits we see in Table 2 are not due to differences in international stock returns but rather are driven by the differences in U.S. stock returns. Also note that the overall EAFE minus U.S. spread was -3.8% over the entire study, the worst of the lot outside of cash. We believe this accounts for the 48% hit rate during active wins; EAFE was such a laggard that its ability to support active managers was tepid at best. The fact that EAFE returns are the same for both active and passive winning timeframes leads us to conclude that the returns of foreign stocks on their own are not a key driver of the active/passive cycle. Cash is the third Index Mismatch asset class. Since equity markets tend to rise over time, cash is a nearly constant drag on active performance. We bring nothing new to the table when we note that cash hurts active managers the most in strong up markets, and near-zero rates today require absolute losses in equities for cash to help at all. Shifting to our analysis of Market Internals, we find a strong storyline develops for some of these factors while others fail to give compelling signals. Value minus Growth has a near-zero average spread over the entire study, but Value trumps Growth by +9.2% when active wins and lags by -3.8% when the index wins. The hit rate is 77% during active wins and 67% during passive wins. The relative spread of Value over Growth is clearly related to active manager wins, and Growth’s recent supremacy is one reason why indexing has been on such a run of late. Our two customized valuation measures fail to deliver strong signals. The Rest minus High P/E had a +1.34% spread over the study and returns are more favorable during active wins. However, the hit rate is no better than random and does not give us much confidence in this indicator. The Rest minus Negative Earners displays a -1.23% spread (silly us, thinking that profitability matters) but the hit rate again fails to inspire confidence. Our first size-focused metric is the Equal-Weighted S&P 500 versus Cap-Weighted S&P 500. Equal weighting has a +0.57% spread overall and outperforms by an average of +4.9% during active manager wins, while it lagged by -4.0% during passive wins. The hit rates of 85% and 77% are among the highest in our study. The Rest minus 25 largest S&P 500 is also very robust. This metric has the highest positive spread over the entire study at +2.71%, meaning that, on average, the 25 largest S&P holdings have underperformed the other 475 over time. The window-specific results are also extremely encouraging with an +11.6% spread during active wins and a -5.8% spread during passive wins, along with very high hit ratios in both columns. Our final size-based factor is the percent of S&P 1500 stocks beating the S&P 500. Return spread is not calculated as this is a ratio-formatted variable, but as we examine the count of S&P 1500 winners we again see encouraging hit rates in both environments. Table 3 shows the granular data on hit rates for each of the eight discrete periods in our analysis. Small Cap minus Large Cap appears robust in seven of the eight periods, with the second passive win timeframe a notable exception (more on this event later).  Chart 2 is a graphical depiction of the percentage of factors in each period that are favorable or beneficial to active management, according to our hypothesis. For example, the chart will have a high reading when most factors support active and a low reading when the factors lean in favor of passive. We’ve shaded the periods when active or passive wins to allow us to compare the headwinds and tailwinds for each. The chart shows a generally confirmatory pattern with higher readings during active wins and lower readings when passive is in favor.

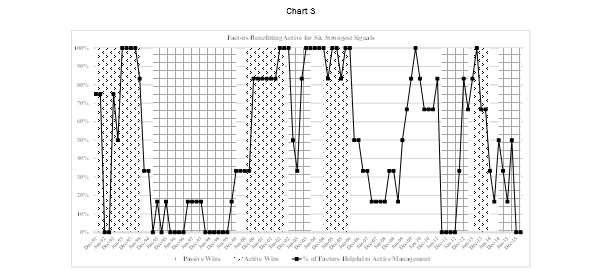

Chart 2 is a graphical depiction of the percentage of factors in each period that are favorable or beneficial to active management, according to our hypothesis. For example, the chart will have a high reading when most factors support active and a low reading when the factors lean in favor of passive. We’ve shaded the periods when active or passive wins to allow us to compare the headwinds and tailwinds for each. The chart shows a generally confirmatory pattern with higher readings during active wins and lower readings when passive is in favor.  The active/passive return cycle does appear to have identifiable drivers that produce the pattern we see in Chart 1. We find the strongest indicators relate to Market Internals, primarily the Mega-Cap effect. The Equally-Weighted S&P 500 measure and our customized Mega-Cap signals, the percent of S&P 1500 beating the S&P 500, and The Rest versus the Top 25, each posted significant return differences during active and passive winning streaks and had the best hit rates in our study. The confirmation provided by each factor convinces us that the primary driver of the active/passive return cycle is the relative performance of Mega-Cap stocks and their impact on the Cap-Weighted S&P 500. We are also struck by the importance of absolute returns for U.S. indexes. The S&P 500 and Russell 1000 indexes registered very different absolute returns during the active win and passive win timeframes. Mid-single-digit returns favor active whereas mid-double-digit returns favor passive. This metric is no doubt influenced by the Mega-Cap effect already noted, yet the sheer simplicity of looking at absolute returns has a distinctive appeal all its own. The Index Mismatch components of our model demonstrate a clear trend, however we are not convinced of the causality behind the numbers. International and Small Cap stocks showed little-to-no difference in return between the two windows of time, suggesting that their contribution to the return cycle is limited at best. Our work suggests that the behavior of international and Small Cap is not inherently different in the winning periods for either style. Rather, the impact of these two variables comes through the relationship they have with U.S. market returns. The apparent spread differences during each category of wins or losses are created by the performance of U.S. stocks, not the divergent performance of Small Cap or international as a driver of relative wins. Value minus Growth does seem to corroborate our thesis by showing clear return spreads and hit rates, however our two customized Value-based measures failed to provide convincing signals. The “P/E greater than 40” and the “Negative Profit” metrics had modest return spreads and uninspiring hit rates near 50%. We believe the Value/Growth relationship is meaningful, but our signals are not nearly as strong as those produced by Mega-Cap indicators. A Refined Set Of Factors Believing that the P/E factors did not provide strong explanatory information, and noting that cash yielding 0% will be a habitually losing asset class, we reconstructed Chart 2 by using the six factors we do believe have a clear and robust ability to account for the active/passive cycle. Chart 3 is a composite of the six strong signals identified by our research, again mapped as a percent of factors favoring active in each return cycle. The chart’s pattern becomes more well-defined and more extreme when we consider just the factors that seem to tell a meaningful story. The data hits maximum and minimum levels on several occasions that correspond well with the active/passive cycle. We think Chart 3 best captures our work and confirms our hypothesis that market conditions and manager tendencies do influence the pattern of relative performance.

The active/passive return cycle does appear to have identifiable drivers that produce the pattern we see in Chart 1. We find the strongest indicators relate to Market Internals, primarily the Mega-Cap effect. The Equally-Weighted S&P 500 measure and our customized Mega-Cap signals, the percent of S&P 1500 beating the S&P 500, and The Rest versus the Top 25, each posted significant return differences during active and passive winning streaks and had the best hit rates in our study. The confirmation provided by each factor convinces us that the primary driver of the active/passive return cycle is the relative performance of Mega-Cap stocks and their impact on the Cap-Weighted S&P 500. We are also struck by the importance of absolute returns for U.S. indexes. The S&P 500 and Russell 1000 indexes registered very different absolute returns during the active win and passive win timeframes. Mid-single-digit returns favor active whereas mid-double-digit returns favor passive. This metric is no doubt influenced by the Mega-Cap effect already noted, yet the sheer simplicity of looking at absolute returns has a distinctive appeal all its own. The Index Mismatch components of our model demonstrate a clear trend, however we are not convinced of the causality behind the numbers. International and Small Cap stocks showed little-to-no difference in return between the two windows of time, suggesting that their contribution to the return cycle is limited at best. Our work suggests that the behavior of international and Small Cap is not inherently different in the winning periods for either style. Rather, the impact of these two variables comes through the relationship they have with U.S. market returns. The apparent spread differences during each category of wins or losses are created by the performance of U.S. stocks, not the divergent performance of Small Cap or international as a driver of relative wins. Value minus Growth does seem to corroborate our thesis by showing clear return spreads and hit rates, however our two customized Value-based measures failed to provide convincing signals. The “P/E greater than 40” and the “Negative Profit” metrics had modest return spreads and uninspiring hit rates near 50%. We believe the Value/Growth relationship is meaningful, but our signals are not nearly as strong as those produced by Mega-Cap indicators. A Refined Set Of Factors Believing that the P/E factors did not provide strong explanatory information, and noting that cash yielding 0% will be a habitually losing asset class, we reconstructed Chart 2 by using the six factors we do believe have a clear and robust ability to account for the active/passive cycle. Chart 3 is a composite of the six strong signals identified by our research, again mapped as a percent of factors favoring active in each return cycle. The chart’s pattern becomes more well-defined and more extreme when we consider just the factors that seem to tell a meaningful story. The data hits maximum and minimum levels on several occasions that correspond well with the active/passive cycle. We think Chart 3 best captures our work and confirms our hypothesis that market conditions and manager tendencies do influence the pattern of relative performance.  A Side Note Seven of the eight time periods generally confirm our hypothesis but one does not fit the mold, in fact it looks rather suspicious. The second passive winning period from 4Q2002 to 1Q2004 shows low hit rates on both Index Mismatch and Market Internals: Size factors, which broadly signal that active should be winning rather than trailing (see Table 3). Note that our favorite characteristic (size and Mega-Caps) performed exceptionally poorly with just one correct sign out of a possible six quarters. After examining this outlier more closely we offer two possible explanations why left is right and up is down in this particular period. First, this window of time contains the snapback following the popping of the tech bubble in 2000-01. During this post-collapse rebound the only modeling signals with high hit rates are the P/E > 40 and money-losing groupings. Curiously, these signals don’t perform well at all during other periods but seem to call the tune in 2002-04. As this study is designed, these results indicate that during this period of index superiority, very high P/E stocks and money-losing stocks were outperforming the middle of the market. These two signals favoring passive management seem to have overwhelmed the other metrics that work so well during the other seven windows. Second, this passive winning stretch is sandwiched between two active winning streaks, and it may be that the rolling twelve-month nature of the data creates noise as the signals transition from one regime to the other. Today’s Weather Active managers are facing a three-club headwind in 2016. Our most recent tally had just two of nine indicators favoring active management, with the most robust indicators’ tally at a rock-bottom zero out of six — no help at all for active managers. Market conditions today favor the passive side of the ledger — conditions as challenging for active management as those that existed during the late-1990s’ tech bubble (see Chart 3 and Table 4). Also note that current five-year cumulative returns include two passive-favorable windows from 2011 to today. Cribbage anyone?

A Side Note Seven of the eight time periods generally confirm our hypothesis but one does not fit the mold, in fact it looks rather suspicious. The second passive winning period from 4Q2002 to 1Q2004 shows low hit rates on both Index Mismatch and Market Internals: Size factors, which broadly signal that active should be winning rather than trailing (see Table 3). Note that our favorite characteristic (size and Mega-Caps) performed exceptionally poorly with just one correct sign out of a possible six quarters. After examining this outlier more closely we offer two possible explanations why left is right and up is down in this particular period. First, this window of time contains the snapback following the popping of the tech bubble in 2000-01. During this post-collapse rebound the only modeling signals with high hit rates are the P/E > 40 and money-losing groupings. Curiously, these signals don’t perform well at all during other periods but seem to call the tune in 2002-04. As this study is designed, these results indicate that during this period of index superiority, very high P/E stocks and money-losing stocks were outperforming the middle of the market. These two signals favoring passive management seem to have overwhelmed the other metrics that work so well during the other seven windows. Second, this passive winning stretch is sandwiched between two active winning streaks, and it may be that the rolling twelve-month nature of the data creates noise as the signals transition from one regime to the other. Today’s Weather Active managers are facing a three-club headwind in 2016. Our most recent tally had just two of nine indicators favoring active management, with the most robust indicators’ tally at a rock-bottom zero out of six — no help at all for active managers. Market conditions today favor the passive side of the ledger — conditions as challenging for active management as those that existed during the late-1990s’ tech bubble (see Chart 3 and Table 4). Also note that current five-year cumulative returns include two passive-favorable windows from 2011 to today. Cribbage anyone?  Does this mean that active management has become a relic, a style no longer to be pursued? Of course not. Markets cycle, styles cycle, environments cycle, and today’s 0-fer tally will change. Size, valuation and breadth will swing and the day will come when most of our active indicators will again be in the green. Active/passive returns will cycle, and the wise investor will avoid concentrating in a winning style during times when it is experiencing unusually favorable weather. “Active and passive” is the right approach; investors should be diligent in identifying their favorite active managers and sticking with those commitments. As surely as today’s weather will change tomorrow (we are in Minnesota, after all) the three-club headwind facing active managers today will turn in their favor once again. Scott Oppsal, CFA, is Director of Research for The Leuthold Group, LLC. His responsibilities include conducting in-depth research projects and exploring fundamental and quantitative studies that support the firm’s portfolio and strategy recommendations. He also coordinates idea flow among the firm’s research team, sits on the firm’s asset allocation and investment strategy committees and is a regular contributor to The Leuthold Group’s institutional research publications. Scott brings over thirty years of professional investment experience to the Leuthold team. As Chief Investment Officer of Invista Capital Management, and as Head of Equities at Members Capital Advisors, he was involved in all aspects of firm management; establishing policies on risk management, asset allocation, quantitative techniques, style-based investing, and taxable investing. He designed and implemented institutional-grade research and portfolio management processes to provide a rigorous, consistent framework for decision making and the analytical tools that drive strategy for multi-asset portfolios.

Does this mean that active management has become a relic, a style no longer to be pursued? Of course not. Markets cycle, styles cycle, environments cycle, and today’s 0-fer tally will change. Size, valuation and breadth will swing and the day will come when most of our active indicators will again be in the green. Active/passive returns will cycle, and the wise investor will avoid concentrating in a winning style during times when it is experiencing unusually favorable weather. “Active and passive” is the right approach; investors should be diligent in identifying their favorite active managers and sticking with those commitments. As surely as today’s weather will change tomorrow (we are in Minnesota, after all) the three-club headwind facing active managers today will turn in their favor once again. Scott Oppsal, CFA, is Director of Research for The Leuthold Group, LLC. His responsibilities include conducting in-depth research projects and exploring fundamental and quantitative studies that support the firm’s portfolio and strategy recommendations. He also coordinates idea flow among the firm’s research team, sits on the firm’s asset allocation and investment strategy committees and is a regular contributor to The Leuthold Group’s institutional research publications. Scott brings over thirty years of professional investment experience to the Leuthold team. As Chief Investment Officer of Invista Capital Management, and as Head of Equities at Members Capital Advisors, he was involved in all aspects of firm management; establishing policies on risk management, asset allocation, quantitative techniques, style-based investing, and taxable investing. He designed and implemented institutional-grade research and portfolio management processes to provide a rigorous, consistent framework for decision making and the analytical tools that drive strategy for multi-asset portfolios.