There has been a flurry in recent days of activity about blockchains among the graybeards of the financial world, those who ponder the Really Big Picture and who have the ear of important regulators.

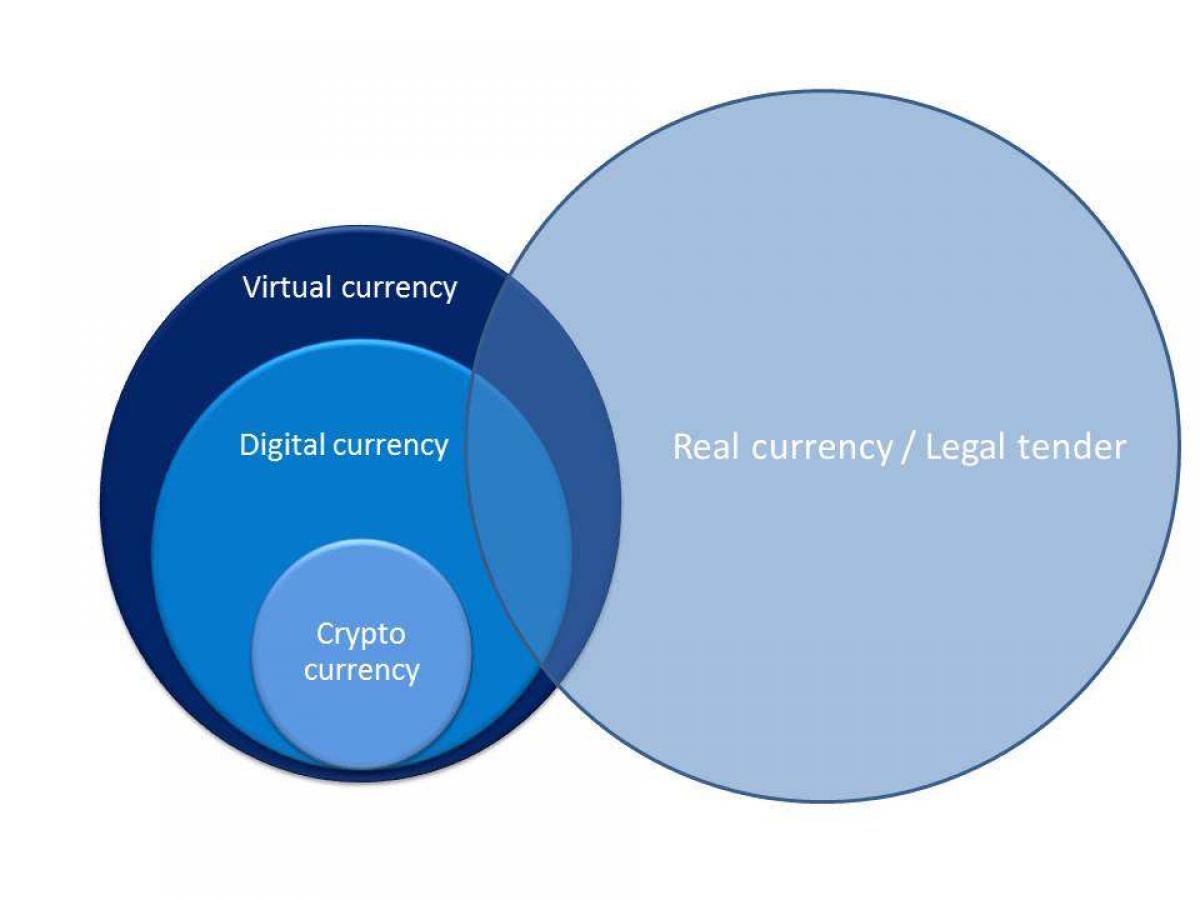

Let us start from the beginning. What is a blockchain? It is a chronological, virtual, and disseminated ledger that covers a history of transactions for a single unit of account. The term arose in the world of bitcoins specifically and alternative currency in general, where a “bitcoin” is a cyber spatial fact that incorporates its own history, going back to the moment when it was “mined.” (For now, let’s leave out of discussion the issue of how mining/creation works.)

One key point is that the blockchain protects the system against digital counterfeiting. Only a bitcoin with a full history, distributed throughout the interested world, is a bitcoin at all.

Blockchains are sometimes known by the longer but more descriptive phrase “distributed ledger technology.”

Financial Applications

It turns out, though, that the blockchain idea has applications well beyond the world of alt currencies. The idea of an ongoing distributed consensus in the online world is exciting. In the words of a paper prepared at UC Berkeley’s Sutardja Center for Entrepreneurship & Technology, the blockchain is a technology that “allows participating entities to know for certain that a digital event has happened by creating an irrefutable record in a public ledger.”

The range of applications includes smart contracts and smart property, meaning that the former can be automatically executed and the latter title verified.

One possibility attracting a lot of attention (prominently featured in the Berkeley white paper for example) is that corporate entities might find it easier to issue shares of their equity directly to the market through blockchains than it is to go the traditional route involving a syndicate of banks. NASDAQ is working with a San Francisco based startup called chain.com to implement PE exchange on top of blockchain.

Greybeards Worry

In this context, then, the greybeards have gotten together before everything gets too disruptive. The European Securities and Markets Authority recently issued a discussion paper on the subject, focusing especially on the application of DLT to the securities markets. The deadline for the submission of comments on the paper has now come and gone.

ESMA speculates thus:

[The] DLT that would be used for financial services would differ from the Blockchain designed for Bitcoins in a number of ways. In particular, while the Bitcoin Blockchain is an open system where all can contribute to the validation process … the DLT that is likely to be used in financial markets would be a permissioned-based system with authorized participants only. This difference is important to keep in mind because it has a number of consequences in terms of potential benefits and risks.

That, frankly, sounds like the voice of a counselor to the threatened authority telling the bosses, “Everything is under control. Reports of disruption are greatly exaggerated.” It is like Polonius telling King Claudius, “Yes, young Hamlet is still furious, but he’ll come around.”

Getting more specific, ESMA has prepared a list of challenges that it believes DLT, even in the tame form it envisions, will face. Scalability, for example: “ESMA is not presently aware of a securities market DLT system useable on a large scale.”

WFE Enters the Fray

The World Federation of Exchanges has responded to ESMA’s thoughts by offering its own. The WFE, the industry association for exchanges and clearing houses, wanted in part to emphasize that Europe isn’t enough. “Due to the global, borderless nature of DLT … global consistency” in regulatory approach is essential to ensure a level playing field and discourage regulatory arbitrage. That can be done, WFE has suggested, either through IOSCO or through the G20.

The WFE also offers a stab at a timeline or, more properly, a range of differing time lines. It says that certain of its members have estimated that the time to market DLT use cases is between 3 to 5 years although there are techno-pessimists among its members who think 10 years is a better guesstimate.

In terms of their own employment of DLT, some WFE members “are at proof-of-concept stage, while others are still somewhere along the spectrum of evaluation, design and proof-of-technology.”

The release of the WFE paper was accompanied by a statement in which the federation’s head of regulatory affairs, Gavin Hill, said that “developments in this space should continue to be market-led and not unnecessarily hampered.”

That, at least, sounds right.