A new paper by Jon Exley, solutions manager of Schroders, discusses cashflow-driven investment (CDI) as a system of portfolio management that accepts and builds upon liability-driven investment (LDI). The idea in both cases is to match all future projected liability payments as they fall due, which is definitionally the imperative of pension funds and the like.

But CDI is not merely a variant on growth-plus-LDI. Rather, in Exley’s formulation, it “involves managing fixed income assets on a buy and maintain (B&M) basis and holding them to maturity, or at least only substituting bonds with the same cashflow profile.”

Back in 1974 Robert Merton designed a model for explaining credit risk premiums. He said that they can be understood as the results for a holder of a corporate bond who sells a put option on the value of the underlying enterprise, with the strike to the put serving as the default threshold of the enterprise.

One can understand CDI through the same theoretical framework. If a portfolio manager is going to hold a certain 10 year corporate bond to maturity, he will know the absolute maximum return that asset can yield, the amount promised. Likewise, he will know the minimum result ($0) in the unhappy event of quick default and unsuccessful recovery. If he holds a number of such bonds, he can add the promised results together and, again, he knows the maximum.

The Arithmetic

Our manager can also know that the difference between the actual outcome and that maximum will be determined by losses on defaults. For a large portfolio of bonds this is “reasonably predictable and can be reserved for relatively easily.” It involves netting out the recoveries one will get on some of those defaults but, again, there is nothing mysterious or especially speculative about the arithmetic. Moody’s data suggests a 40% recovery on defaults.

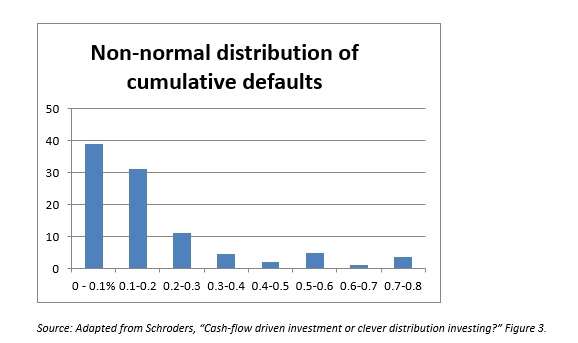

The paper includes a graph on the distribution of cumulative defaults over ten-year rolling periods. In nearly 40% of the periods studied (over the last 90 years) bond defaults have stayed at or below 0.1%.

The credit spread, that is, the premium earned by selling the hypothetical put in the Merton model as explained above, will on average exceed the expected loss in the underlying asset, the equities. This is true regardless of whether or not volatility itself is earning a premium and regardless of whether or not there is a skew in the volatility assumption.

This feature of the model means that the expected losses on default will be below the premium earned, which is where one wants it.

Dynamic Flight Plans

Exley also discusses managers who reduce or plan to reduce their growth assets dynamically, either in response to improved funding or systematically through the passage of time. These strategies are known as “flight plans” in the hope of a smooth landing. He shows that managing traditional assets with a flight plan makes them behave like a CDI solution. The payout model of a flight plan strategy shares with CDI the capped upside, the improved certainty of outcome in central scenarios, and the continued exposure to significant downside risk in the more extreme scenario.

Exley contends that despite the similarity “there are a number of significant advantages” that CDI possess over a flight plan strategy. The target outcomes of the CDI solutions are less dependent than that of the flight plans on unknowns, and the triggers for flight plans can create cliff edge effects, depending on whether a target level has been just hit or just missed. In general, too, “the governance requirements of monitoring flight plans are significantly more onerous than those of CDI solutions, which are relatively straightforward.”

Nonetheless, Exley expects that CDIs and flight plan strategies will fold into one another over time. Flight plans are popular for higher return targets and CDI solutions for “less ambitious targets,” which suggests “a natural two-stage evolution which sees both risk and governance burden decline as the solution develops over time.”

The paper ends with some fine print stating the usual disclaimers. “The views and opinions contained within” are those of Mr. Exley, not those of Schroders as a corporate entity.