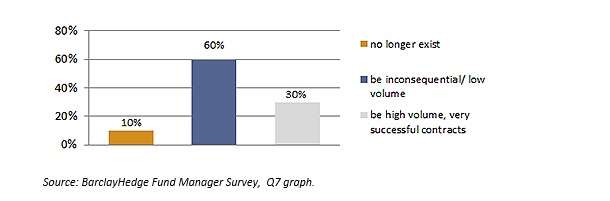

A new BarclayHedge study indicates that the majority of commodity trading advisers surveyed are unenthusiastic about the new Bitcoin futures. Specifically, asked “do you consider Bitcoin futures to be a valuable/useful addition to a diversified futures portfolio?” nearly three quarters (73%) said “no.” The sample for this survey included firms located in the U.S., the U.K., Switzerland, Canada, and Japan. Asked whether they believed that these futures would become very successful, high volume contracts within a year 60% said “no,” and another 10% said they would no longer even exist within a year. This leaves only 30% of the opinion that they will be high volume.  Combining these two facts and some arithmetic: the 70% who believe either that these futures will be marginal products in a year or that they won’t exist at all closely corresponds to the 73% who said they aren’t valuable or useful. This looks like an unintended endorsement of the hypothesis of efficient capital markets. An opponent of the ECMH might believe and argue both that they are useless and that they will be high volume in a year’s time, since such an opponent can believe that irrational faddishness would make it so. A Fair Chance to Prove Itself On the other hand, if one is part of the minority that believes that bitcoin does serve a valuable purpose and will prove itself in the market over time, the survey gives one also some ammunition. Asked whether they are already trading Bitcoin futures, only 5% said “yes.” But when those who said “no” (the 95%) were asked if they intended to do so within the next six months “as these contracts develop,” the affirmative answer rose to 19%. That may be enough to make for a proving ground. Nineteen percent of 95% gives us 18% to add to the original 5% of active traders. Adding those who now trade these products to those who say they will within six months gives us 23% of the whole, which may be enough to constitute a fair proving ground. Among those who are interested in trading Bitcoin futures, the CME has the inside track. When the CTAs were asked on which of the two exchanges involved they are most likely to do such trading, 25% said the CME. Only 4% said the CBOE. Another 15% said “both,” leaving a majority (56%) still undecided. The Crash All new futures contracts, along with surveys and opinions about them, come amid news of a Bitcoin crash, hat CNBC calls “Crypto Carnage.” A single Bitcoin was worth $19,800 at the peak in mid-December. On Tuesday afternoon, January 16, only a month after that peak, it was briefly below $10,000 on Coinbase. This means (simple arithmetic again) its value fell by nearly half. Does this mean the “bubble has burst” and that Bitcoins will soon go the way of pet rocks? Not at all. Bitcoin has endured crashes before. Indeed, the boom-bust pattern has been integral to its growth as it has over the years cemented its position as the flagship of the cryptocurrency fleet. There was a speculation-driven upward move in Bitcoin value in November 2013 that took it from $280 to $945. It was then, within sight of passing the $1,000 mark, that Bitcoin suffered what seemed to many at the time a fatal reverse. Sixteen months later it was at $270, below its value at the start of that November run-up. But of course Bitcoin didn’t go away. It stuck around in that $200-$300 basement for a while, then early in 2017 began the rise that would eventually dwarf that earlier exciting-at-the-time trip. Bulls will argue that the cryptos in general have found a firm and practical role in the finance world, because they offer themselves as a medium of exchange that is self-executing, transparent, and independent of the whims of central bankers. That futures are available itself confirms this premise, however much CTAs may be (understandably) wary. A Final Thought With regard to the choice between CME and CBOE referenced above, BarclayHedge observes that in the week beginning January 8, 2018, there were 6,030 Bitcoin futures traded on the CME’s Globex market. In the same week the CBOE volume was more than four times that: 24,610.

Combining these two facts and some arithmetic: the 70% who believe either that these futures will be marginal products in a year or that they won’t exist at all closely corresponds to the 73% who said they aren’t valuable or useful. This looks like an unintended endorsement of the hypothesis of efficient capital markets. An opponent of the ECMH might believe and argue both that they are useless and that they will be high volume in a year’s time, since such an opponent can believe that irrational faddishness would make it so. A Fair Chance to Prove Itself On the other hand, if one is part of the minority that believes that bitcoin does serve a valuable purpose and will prove itself in the market over time, the survey gives one also some ammunition. Asked whether they are already trading Bitcoin futures, only 5% said “yes.” But when those who said “no” (the 95%) were asked if they intended to do so within the next six months “as these contracts develop,” the affirmative answer rose to 19%. That may be enough to make for a proving ground. Nineteen percent of 95% gives us 18% to add to the original 5% of active traders. Adding those who now trade these products to those who say they will within six months gives us 23% of the whole, which may be enough to constitute a fair proving ground. Among those who are interested in trading Bitcoin futures, the CME has the inside track. When the CTAs were asked on which of the two exchanges involved they are most likely to do such trading, 25% said the CME. Only 4% said the CBOE. Another 15% said “both,” leaving a majority (56%) still undecided. The Crash All new futures contracts, along with surveys and opinions about them, come amid news of a Bitcoin crash, hat CNBC calls “Crypto Carnage.” A single Bitcoin was worth $19,800 at the peak in mid-December. On Tuesday afternoon, January 16, only a month after that peak, it was briefly below $10,000 on Coinbase. This means (simple arithmetic again) its value fell by nearly half. Does this mean the “bubble has burst” and that Bitcoins will soon go the way of pet rocks? Not at all. Bitcoin has endured crashes before. Indeed, the boom-bust pattern has been integral to its growth as it has over the years cemented its position as the flagship of the cryptocurrency fleet. There was a speculation-driven upward move in Bitcoin value in November 2013 that took it from $280 to $945. It was then, within sight of passing the $1,000 mark, that Bitcoin suffered what seemed to many at the time a fatal reverse. Sixteen months later it was at $270, below its value at the start of that November run-up. But of course Bitcoin didn’t go away. It stuck around in that $200-$300 basement for a while, then early in 2017 began the rise that would eventually dwarf that earlier exciting-at-the-time trip. Bulls will argue that the cryptos in general have found a firm and practical role in the finance world, because they offer themselves as a medium of exchange that is self-executing, transparent, and independent of the whims of central bankers. That futures are available itself confirms this premise, however much CTAs may be (understandably) wary. A Final Thought With regard to the choice between CME and CBOE referenced above, BarclayHedge observes that in the week beginning January 8, 2018, there were 6,030 Bitcoin futures traded on the CME’s Globex market. In the same week the CBOE volume was more than four times that: 24,610.

Search

Search Close

Close