By Diane Harrison

It’s human nature to want to keep on getting more of what seems good, but is piling on always the right call? Obviously not, as too much of anything can turn good to bad. Overeating, over exercising, over working all can tip one from engaging in a good activity into forming a bad habit. Investment managers are only human, and can fall prey to the same vagrancies anyone else might, including decisions that negatively impact their own business. Following are some watch items to be cognizant of when attempting to work harder in the fund management world.

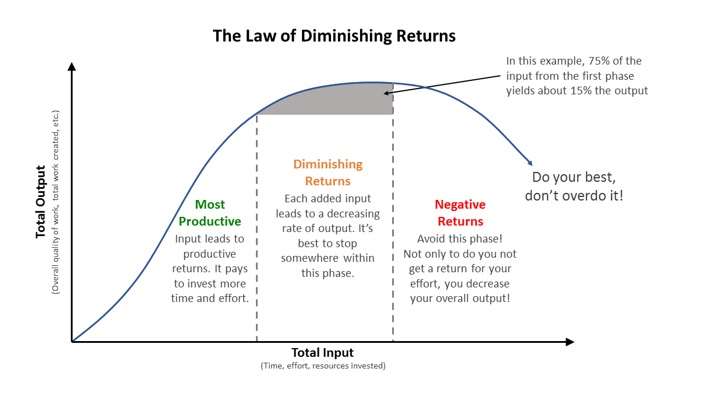

THE LAW OF DIMINISHING RETURNS

Encyclopedia Britannica defines the law of diminishing returns as an economic law stating that if one input in the production of a commodity is increased while all other inputs are held fixed, a point will eventually be reached at which additions of the input yield progressively smaller, or diminishing, increases in output.

In other words, you can veer too far in the quest for more only to receive less.

Source: pmctraining.com

What does this mean for fund managers? Being aware of limited resources, limited capital, and limited time to focus on key activities requires a manager to…well…manage time and resources wisely to attain maximum results on a range of fronts. There’s literally no time for managers comfortable with wading through mountains of investment data to get caught in the weeds of management minutiae. Here are five key areas that managers want to keep an eye on to avoid "effort overreach."

Investment Management

As the lifeblood of any funds management business, priority of time and resources should be devoted to this area regardless of firm size. If the investment strategy requires a significant investment in human research, computer programming, or other statistical analysis, then resources required for the other non-investment areas must be trimmed to accommodate the allocation of time and money to this function.

Without the highest quality efforts devoted to optimizing investment and research, performance will undoubtedly suffer, and jeopardize the long-term success of a fund business. Managers know this, and rarely skimp on resource allocation to this area. However, there must be sufficient time and capital allocated to the other four in support of this key function, or the business will suffer regardless.

Marketing Outreach

In order to stay in business, a fund needs to grow. It’s possible to grow solely through organic expansion via performance and infusions of capital from existing partners, but typically a fund reaches a point in its lifecycle where it needs to add new capital from outside to remain successful. Attracting clients, particularly when you are a small or niche fund, takes time, effort, and persistence. There are many roadblocks to doing this, but gathering assets is a numbers game and requires perseverance. “Procrastination is the devil in startups. So no matter what you do, you gotta keep that ship moving.” — Ron Conway, Founder of SV Angel, an angel investor in startups.

But keeping the ship moving is not a recipe for success in itself. Targeting the right prospects, contacting the right decision-makers, and delivering effective messages all work in concert to win over new money. As important to doing these things right is to avoid wasting time trying to do these activities with the wrong target base or non-decision makers. Practice makes perfect when learning to distinguish between the two.

Operational Efforts

New funds are often run as lean and mean on the personnel side as possible, as one of the biggest expenses in a startup fund is key talent. But the need for qualified people is even greater when every internal position is performing essential tasks. Outsourcing some or most back-office functions offers the potential to deliver high-quality operational functions such as fund administration, accounting, legal and compliance, and also to avoid the risk of a ‘key-man’ exit disruption negatively impacting the fund business.

Multiple outsource roles are available to take over essential functions, with minimal impact to processing and reporting. For fund managers with limited ability to hire and retain senior people at the early stages of the business, being able to employ ‘fractional’ experts, as they are referred to, in roles such as CFO, Chief Compliance Officer, and Chief Information Officer offers these funds a greater opportunity to compete for new clients against larger competitors.

Investor Relations

In 2002, the passing of the Sarbanes-Oxley Act, otherwise known as the Public Company Accounting Reform and Investor Protection Act, significantly impacted the frequency and depth of the financial information on which publicly-traded companies were required to report. This pressure to become more transparent spilled over into the private placement world as well, creating an ever greater need for consistent and meaningful investor relations efforts in the alternative assets sector.

Effective and honest communication with all investors—limited partners in a fund, separately managed accounts and others—is the primary goal of investor relations. Performance is one piece of the communication channel, but not the only. Firm goals and values, management updates on the firm’s non-investment business activities, investment manager outlooks impacting the direction of business focus all weigh into the communication messaging that provides outsiders with a better view into the workings of a fund.

Brand Building

Another key activity that can fall by the wayside of resource-strapped managers is the creation, protection, and reinforcement of a firm’s brand. Financial clients absolutely require their investment partners to demonstrate trust, reliability, and a solid reputation in order to invest with them. Brand management, while intangible, is an integral part of this relationship. Marrying what you do with what you say and how others perceive you are, in essence, the heart of brand building.

A distinctive logo, memorable tagline, and consistent imaging and tone throughout all firm communications work together to define and reinforce a firm’s brand. While supervising the creation of a logo, tagline, and brand identity standards program is a task managers understand and can execute, most fund managers are unfamiliar with the necessary actions to coordinate these elements on an ongoing basis through all external touches with clients and prospects. Client statements, investor communications, marketing collateral, websites, and thought leadership activities such as articles, speeches, white papers, and the like are also key pieces of a firm’s brand building.

Strong branding creates client loyalty. Taken as a whole, the individual activities of brand building forge a memorable impression of a business on its target market. Branding can help build up a company through positive association and create a resiliency towards difficult market times that assist a fund business in retaining loyal clients. It’s too important to ignore.

Diane Harrison is principal and owner of Panegyric Marketing, a strategic marketing communications firm founded in 2002 specializing in alternative assets. She has over 25 years’ of expertise in hedge fund and private equity marketing, investor relations, articles, white papers, blog posts, and other thought leadership deliverables.