Austin Shelton, a Ph.D. candidate at the University of Arizona, has applied quantitative rigor to the question of how stop-loss and stop-gain rules, even simplistically formulated rules, can assist the risk-adjusted return of a portfolio.

Austin Shelton, a Ph.D. candidate at the University of Arizona, has applied quantitative rigor to the question of how stop-loss and stop-gain rules, even simplistically formulated rules, can assist the risk-adjusted return of a portfolio.

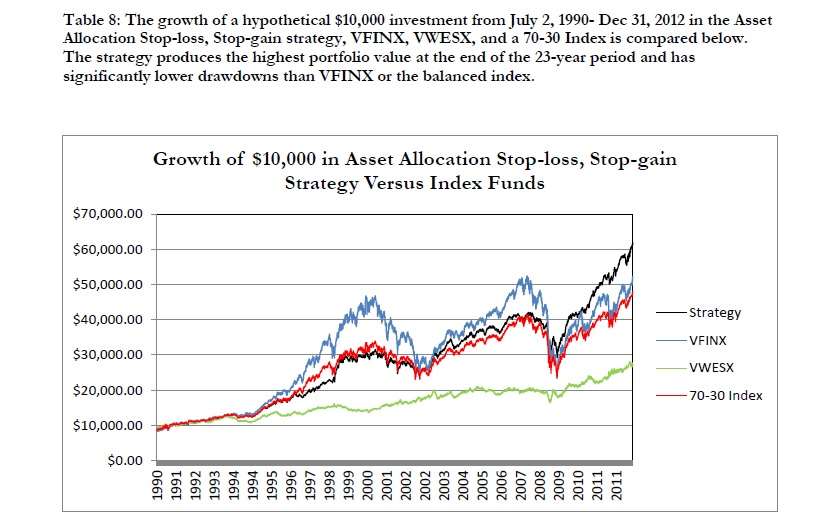

Shelton tracked a hypothetical $10,000 portfolio as it would have performed from July 2, 1990 until December 31, 2012 employing four distinct strategies. As you can see from the graph below, the race is won by the genetically engineered turtle Shelton has created, the “asset allocation stop-loss, stop-gain strategy,” which we might more tersely just call the black line.

It took the crisis of 2007-08 to put this turtle in the lead, though. The same chart shows that until then, over a considerable period, the VFINX (the Vanguard 500 Index Fund) was clearly ahead. Also, until that same crisis, the 70-30 Index tracked the Stop-Loss quite closely. As one might expect, the very conservative Vanguard long-term government bond index, VWESX, stays in the basement throughout the period covered in this graph.

But to get back to the initial point: what exactly is the Stop-Loss strategy reflected in that black line that’s at the top on the right-hand edge of the graph? Shelton has used just two assets to create it: those two assets are VFINX and VWESX as defined above.

Stop Rules as Asset Shifters

Stop-loss and stop-gain rules constitute the only method of shifting assets from one half of this hypothetical winning portfolio to the other. There is no asset shifting based on “inferences regarding expected return or even expected variance.”

The 70-30 index also used for purposes of comparison is a less dynamic combination of the same two underlying assets: 70% VFINX and 30% VWESX.

The results for that 70/30 mix are as follows:

Annual Geometric Return: 7.16%

Annual Arithmetic Return: 7.71%

Annualized Standard Deviation: 12.98%

Information Ratio: 0.55

The same vital statistics for the Stop-loss model are:

Annual Geometric Return: 8.45%

Annual Arithmetic Return: 9.01%

Annualized Standard Deviation: 9.41%

Information Ratio: 0.90.

Thus, the stop-loss model recorded better results and lower volatility. The real benefit of this strategy, as Shelton sees it, is the decrease in portfolio variance it creates relative to investment either in the balanced index or in a straight equity portfolio.

Crisis and Correlations

While making this point, Shelton quarrels with the cliché that “in a crisis, correlations all go to zero.” The significance of a two-asset, equity/debt model of course depends upon the underlying fact that equity and fixed-income instruments are not correlated. What was that about a crisis?

In 2008, both VWESX and VFINX were down, but there wasn’t a very close correlation. Specifically, VWESX returned an unlovely -2.46%, while VFIND returned a horrific -36.66%.

In 2001, the year of the 9/11 attacks and the sudden collapse of Enron, VFINX returned -11.28%. But VWESX returned +5.74%. Here again, nothing like “correlation going to one.”

How would Shelton’s new proposed strategy have done for an investor in each of those two crisis years? In 2008 it was down: -17%. So it didn’t preserve value as effectively as the government-securities index, but did a better job than did the 70/30 portfolio, which was down that year 26.40%.

In 2001, on the other hand, the Stop-Loss strategy was down slightly more than the 70/30 balance was [6.40% versus 6.17%.]

Bottom Line

Shelton calculates that his strategy has “a statistically significant CAPM alpha of roughly 2 bp a day, 40 bp a month, or around 4.84% a year,” and he calls this “quite amazing for a strategy that simply moves assets between stock and bond funds based on pre-defined, fixed stop rules.”

But this brings us to the question of robustness. The Stop-Loss strategy as Shelton envisages it requires certain exogenous inputs: the number of stop loss levels, the number of stop gain levels, and the spreads between the chosen loss and gain levels. Shelton checked robustness by re-specifying these inputs while leaving unchanged the underlying database and strategy.

All 16 tested re-specifications agreed with the original specification in showing significantly less variance than the 70/30 fund. Also, 14 of the re-specifications beat the raw return of that balanced index, and 12 of them beat the raw return of VFINX.

His conclusion is that “asset allocation strategies that incorporate stop-loss and stop-gain rules may indeed offer a valid alternative to passive long-term investing.”