A recent survey of firm-valuation experts from 10 European countries indicates that they can produce wildly different values given the same inputs.

A recent survey of firm-valuation experts from 10 European countries indicates that they can produce wildly different values given the same inputs.

Okay: maybe that’s not too surprising. Any valuation model will necessarily include parameters that will in turn require a best-guess approach, often as subjective in inspiration as it is objective in aspiration. So valuations will differ. Also, there is a choice between models: discounted cash flow or relative valuation? Or something a little less run-of-the-mill, such as the option valuation framework?

If an expert decides upon the discounted cash flow model, there is still a choice to be made among variants. Is he looking for free cash flow to the firm or free cash flow to the equity?

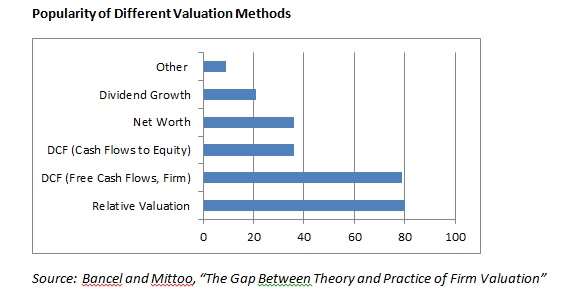

According to the survey, the popularity of various valuation measures among respondents breaks down as follows:

The numbers obviously don’t add up to 100%, because many (indeed most) of those whose business it is to assign a value to privately owned firms employ a mix of methods.

Relative Value

You’ll see that the aforementioned option valuation framework, which has some academic cachet, is here part of the generic “others” category, and sees little use.

Let’s focus on the item at the bottom of that list, “relative value,” for a moment. On this method, the valuers find a publicly owned firm that, or group thereof, that is a peer/analog of the private firm that they’ve been hired to value. They work from the market’s valuation of the peer, with the help of a multiple.

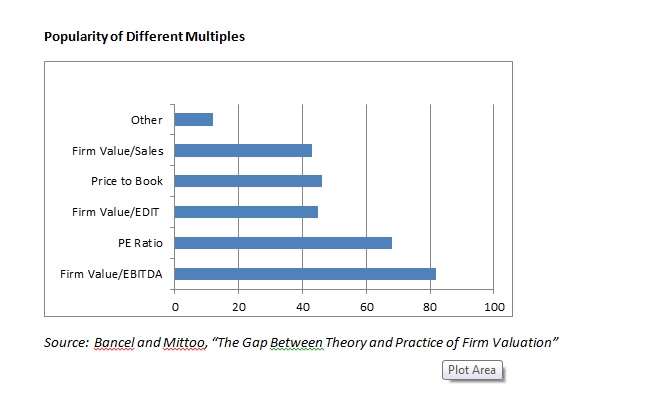

Selection of the peer or peer group can itself be a somewhat subjective matter. But the authors of a report on this survey focus on the other parameter here: the multiple. Which multiple?

“The academic and professional textbooks,” they say, “maintain several choices” such as price-to-book, firm value to EBITDA, price to earnings, etc. The most frequently used of these methods by practitioners is firm value to EBITDA.

At any rate, you dear reader are probably not surprised that the valuation experts often disagree. What may be a little surprising, though, is that according to the authors of a report on this survey, at least some of the disparities in valuation (for a constant set of input) arise because the expert practitioners often simply ignore adjustments in their calculations, even when those adjustments are clearly called for by the capital asset pricing model, the model that provides the theoretical infrastructure for both RV and DCF.

Franck Bancel, professor of finance at ESCP Europe, and Usha R. Mittoo, of the Department of Accounting and Finance and the University of Manitoba, say for example that while CAPM calls for “forward-looking betas and risk premiums, less than half of practitioners make such adjustments.”

They also note, specifically with reference to the RV framework, that many of its practitioners specifically reject the underlying theoretical assumption of the method when it is made explicit. RV presumes that financial markets are efficient, so that the peer companies are fairly valued. But when respondents are asked whether they agree with that assumption, “about one-third of respondents question the validity of RV approach despite using it.”

Nation of Origin and a Final Inference

The largest group of their practitioners/respondents comes from France (36%). They also have significant participation from the UK, Spain, and Switzerland (16%, 13%, and 12% respectively).

One inference that Bancel and Mittoo don’t explicitly draw from their data, but I will because this is AllAboutAlpha, is that there is a lot of alpha to be found in the woods of privately-owned companies. After all, with this wide range of ‘right’ answers for the simple-seeming question of “what is this company worth,” somebody is surely selling for less than they could.