By Rick Ehrhart, JD

By Rick Ehrhart, JD

A long-standing drawback of hedge fund incentive compensation has finally reached a breakthrough. The traditional incentive compensation model short-changes institutional investors. It allows portfolio managers in a hedge fund to receive incentive compensation on a quarterly or annual basis while investors had to wait until redemption day to realize either an aggregate gain or loss. This mismatching of incentive goals gave the manager a disproportionate share of the 80/20% incentive compensation split over the life of the investment relationship, ultimately “punishing” the investor for remaining committed to the investment on a longer-term basis. With the vast majority well north of 90% of institutional investors committed to their hedge fund investment for at least three years and often for longer than 5 years, this misalignment in incentives payment causes a real value disparity in the mutual experience of hedge fund manager versus hedge fund investor within the same pool of funding.

WHAT HAS CHANGED THIS IMBALANCE?

U.S. law, for one. The IRS just issued a revenue ruling, 2014-18, on June 10, 2014, that allows hedge funds the ability to provide incentive compensation in the form of fair market value (FMV) options or stock appreciation rights (“SARs”). This new ruling clarifies that stock options and stock-settled stock appreciation rights (SARs), properly designed, can be used as a form of compensation to managers of offshore hedge funds and other “nonqualified entities” under Internal Revenue Code Section 457A (“Section 457A”).

An elegant solution to the traditional compensation alignment problem is to deliver the manager’s incentive fee in the form of a stock option or stock-settled SAR, with a grant price equal to the fair market value of the fund shares on the date of grant. The manager does not realize value from the stock option/SAR until it is exercised.

With this new ruling, investors finally have the ability to ask their hedge fund manager to literally “put their money on the line” in a pari passu relationship that places both manager and investor on a level field. FMV options/SARs divide cumulative tax-deferred profits over the life of the investment and will ultimately create the alignment of long-term interests that has been lacking in the current performance model.

First, a brief tax code overview is useful to summarize where things stood in terms of the uncertainty surrounding what exactly constitutes “deferred compensation” subject to an annual realization for taxable purposes. In 2004, Congress enacted 409A to regulate deferred compensation earned by any U.S. taxpayer. In the course of developing its comprehensive regulatory regime for 409A, the Treasury and the IRS struggled with whether stock options should be included in the definition of deferred compensation. The concern centered on the potential for stock options to be used as a form of “disguised” deferred compensation. As a result, the 409A regulations include very specific requirements for a stock option not to be considered “deferred compensation:”

- The stock option is granted with respect to “service recipient stock;”

- The stock option is granted by an “eligible issuer of service recipient stock;”

- The compensation payable upon exercise of cannot be greater than the excess of the fair market value (FMV) of the stock at exercise over the FMV of the stock when the option is granted, and the number of shares of underlying stock is fixed at grant;

- The strike price can never be less than the FMV of the stock at the grant;

- The option does not include any other feature for the deferral of compensation.

Congress enacted 457A in 2008. Section 457A prohibits “tax indifferent” entities – such as offshore funds located in “tax havens” or domestic funds organized as partnerships and with significant ownership by tax-exempt entities – from providing deferred compensation to its service providers, such as an investment manager. Under Section 457A, compensation must generally be recognized on an accrual basis. If compensation under an arrangement cannot be determined annually, it will be taxed when it can be determined and, in that case, will be subject to a 20% penalty. 457A seemingly forces funds into annual incentive compensation arrangements rather than long-term performance-based programs.

In Notice 2009-8, the IRS instructed that 457A does not apply to stock options that otherwise meet the requirements of the 409A regulations. Despite Notice 2009-8, a few influential hedge fund lawyers thought there was uncertainty about whether hedge fund managers could avail themselves of options/SARs.

BREAKING THE SILENCE AT LAST

The June 10, 2014 revenue ruling clarifies that Section 457A does not apply to FMV options/SARs issued by private investment funds such as hedge funds. The law has long recognized that deferred compensation and stock options are different. When a service provider defers income, the income is crystallized and not subject to subsequent performance of any capital other than the crystallized income. The benefits from stock options are not crystallized until the options are exercised. Moreover, the benefits are leveraged, which means they are subject to the performance of not only the benefits, but the leverage amount, of the capital. The implication of the ruling makes clear that funds can issue FMV options/SARs without tax risk. We at Optcapital like to call this outcome the genesis of Fund Alignment Rights®, or FAR, as it finally allows both hedge fund managers and investors to align their long-term interests in the investment on a level tax-considered basis.

Instead of crystallizing the manager’s share of profits each year, or each quarter as some funds do, the fund can crystallize the manager’s share at the same time that the investor crystallizes, or earlier if the investor agrees. Options keep all assets (and profits) invested and compounding pre-tax, tax-deferred until the parties crystallize, after 3 years, 5 years, or longer. This represents true, side-by-side sharing of cumulative profits.

Even though options are not deferred compensation, they are tax-deferred until exercised. This means that most managers will accumulate substantially greater wealth from options than from annual crystallization (which means annual taxation and investment growth at an after-tax rate). With tax rates above 50%, deferring taxation is very attractive.

HOW DOES THE FUND ALIGNMENT RIGHTS PROCESS WORK?

Let’s assume that, instead of paying the manager each year based on annual profits, the fund could pay the manager using fair market value options. How end-of-performance sharing works with FMV options:

- To share cumulative, terminal profits 80%/20%, the fund grants manager an option to purchase 20% of shares at strike price equal to NAV of shares at date of grant.

- The option gives the manager all the profits on 20% of the shares whenever the option is exercised.

- Until the option is exercised, the manager is not taxable on its share of the profits.

- There is no time limit on the exercise of the option. And the option can be exercised in all or in part, with the balance remaining in the fund to compound pre-tax, tax-deferred.

- All the assets (the investor’s and the manager’s) remain invested side-by-side, without erosion from fee banking or taxes, until the option is exercised.

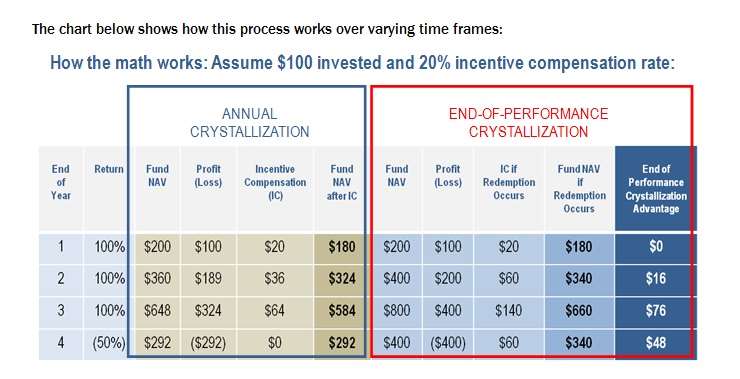

FMV options divide cumulative, pre-tax profits at the end of the life of the investment – i.e., deferred profit sharing. Investors and managers always receive their proportionate share of profits and losses. In addition, the manager can increase its after-tax capital accumulation by taking full advantage of compounding at a pre-tax, tax-deferred rate and the power of time. Based on historical averages of a sampling of top hedge funds, a 10-year investment under a deferred profit sharing model would increase annualized returns by more than 2.0% and investor assets by more than $1 billion on every $1 billion invested. Multi-year investors always receive more from deferred profit sharing, whether the fund is up or down.

With deferred profit sharing, the division of profits is tentative until redemption, at which time the profits are divided 80/20. Consequently, there is an inherent claw back mechanism that ensures that the manager participates in losses. The incremental return for investors is what Optcapital refers to as “alignment alpha®.”

As this chart shows, the numbers clearly illustrate the benefits of this longer-term focus on the ultimate NAV values for the fund over both positive and negative performance periods.

FMV options offer genuine advantages for managers as well as investors. By aligning the interests of both investors and managers, managers can experience:

- Greater capital accumulation (with the inherent tax advantages of deferring taxable events in the compensation payments).

- Enhanced attraction and retention of ‘sticky’ institutional capital (through promoting a longer-term, mutually advantageous relationship with key investors).

- A better business model (management companies build a pool of pre tax “retained earnings” to draw down as needed).

- Enhanced retention of key alpha generators (a sort of ‘retention insurance’ to incentivize key personnel to remain with the firm through longer-term compensation arrangements).

THE CLAW BACK DRAWBACK CAN BE A THING OF THE PAST

Investors seek alignment during the course of a drawdown. Under the current incentive payment environment, institutional investors typically negotiate a one-off deal with each manager that, in effect, gives the manager just enough of his incentive fee every year to pay taxes (about 45% of the fee) and that allows the manager to leave the rest or set aside the rest for a period of time as subject to claw back in the event of a subsequent drawdown. That leaves approximately 55% of the fee in the fund or segregated to be subject to claw back.

The greatest disadvantage of the partial payment arrangement is that whatever the manager pays in taxes is not subject to investor claw back. At most the investor could look to claw back 55% rather than the 100% of what using FMV option under a FAR relationship arrangement allows. Creating the worst of both worlds, the manager also loses the ability to realize a prospective return on the capital used to pay those taxes.

This one-off negotiation is tedious and complicated for institutional investors to track and manage. With this clarification on the new ruling and the implementation of a Fund Alignment Rights® structure instead, investors will no longer need to bother with the tracking of partial payments for tax and hold backs, etc. The manager can defer and compound all of his incentive earnings, so both parties benefit from the use of FMV options.

A BETTER DEAL FOR ALL

The mathematics of the longer term deferment shows the obvious advantage of Fund Alignment Rights® by using FMV options as part of the compensation structure between hedge fund managers and investors. In addition to the economics, there are important benefits that present themselves in conjunction with a FAR relationship between managers and investors, including:

- Aligned interests

Investors can rest assured that the manager and incented employees will be focused on realizing the highest pre-tax returns for the life of the investor’s shares supporting the option.Managers can promote their commitment to prospective investors to managing the fund assets to the aggregate benefit of all, through participating in both the profits and losses on incentive compensation accrual. This arrangement lessens the current investor perception shared by many that annual management fee income is the primary driver of running a hedge fund business, particularly in years where incentive performance is less than anticipated.

- Longer-term relationships between investors and managers

Withthe focus on the total lifespan of the investor relationship, with a performance crystallization date in the future, there is no uncertainty around interim valuations that might otherwise drive annual performance fees acrimony. Managers and investors can focus on the fund strategy and market opportunity exploitation, and spend less time negotiating one-off fee structures. The removal of the annual incentive payment adjustment to the investment may help to further the mutual understanding of long-term goal attainment for both sides of the relationship, and to promote communication between both parties.

- Ability for managers to attract larger investors

Established managers can use FARs tactically to secure separate managed account allocations from institutional prospects, or simply create a FAR fund for a particular like-minded target market segment (such as endowments). Smaller and emerging managers can use the FAR relationship construct to assist them in attracting larger investors to their fund by effectively reducing the implied risk that these investors perceive of placing their money with a newer or start-up fund. By agreeing to defer the incentive compensation and putting more of their “skin in the game,” managers may have an easier time convincing new institutional investors that they are committed to growing a business for the long term, and not for a short-term gain. Similarly, institutional investors, who have long faced a shortfall in meeting their investment portfolio performance objectives, will have a wider pool of investment talent within which to seek this performance.

- Fewer side letter deals

Managers seeking to land a relationship with the larger institutional investors will have the ability to offer a tailored FAR structure to these prospects, minimizing their need to agree to independent side letter, or pocket deals. This will help to streamline the fund administration process for hedge fund managers, as well as reduce the future impact of a side letter deal to one creating a most-favored nation status for future institutional investors.

We at Optcapital are excited about the revenue ruling that has finally made this alignment of interests a viable and mutually beneficial arrangement for hedge fund managers and investors alike. With the clarification of this ruling, investors can now ask for, and managers can now offer, Fund Alignment Rights® with the use of FMV options/SARs to their investors that serve a long-term advantage to all.

Rick Ehrhart, JD is President and CEO of Optcapital. Rick began his career practicing law, first as an antitrust litigator and then specializing in executive compensation. Rick is a member of the American Bar Association, North Carolina State Bar, and American Association of Justice. With his partner, Bob Avinger, Ph.D., he founded Optcapital in 1998. The firm started as a joint venture with Wachovia Bank to provide a new and better type of deferred compensation to Fortune 1000 executives. Optcapital’s mission is to provide elegant complete solutions. The firm’s hallmark has been innovations that offer superior investment control, liquidity, and flexibility with respect to the timing of benefits. Today, Optcapital administers more than $3 billion of deferred and incentive compensation, including FMV options/SARs.For more information, please contact Rick.Ehrhart@optcapital.com.