Hedge fund managers and investors see eye-to-eye on some important subjects, according to a survey by Northern Trust.

Hedge fund managers and investors see eye-to-eye on some important subjects, according to a survey by Northern Trust.

But the same survey also cautions: there is a termite in the firewood. The two groups don’t see at all eye-to-eye on transparency.

First, the good news. Managers and investors are agreed that hiring the right people is a top priority for the industry looking ahead. Almost half of managers (45%), and a little more than half of the investors (56%), see the recruitment and retention of talent as a high priority, either the first or the second item on their respective lists. But leave aside this “top two” stuff and consider only #1. Forty-one percent of investors of the largest hedge funds, those with $1 billion or more in assets under management, cited personnel issues as their #1 priority.

Funds by Size and Region

Likewise, there is consensus about product development. Roughly a third of each group ranked product development as a top-two priority (investors, 32%: managers, 39%).

On the subject of the impact of recent regulations, too, there is some agreement between managers and investors in the industry. A majority of managers (59%) and a somewhat smaller majority of investors (53%) believe that regulations have greatly reduced the likelihood and severity of another financial crisis. There remain skeptics in the industry, on both sides of that equation. Forty percent of investors and 34% of managers deny that regulations have done anything to avert a future crisis.

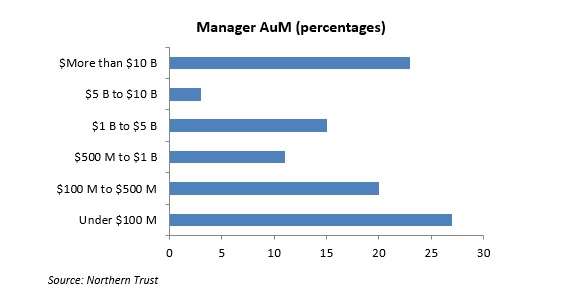

Who are these respondents? On the managerial side, they came from 117 different funds, and 49 of those funds have AUMs of $1 billion or more. Twenty-seven of those funds have AUMs about $10 billion.

In percentage terms, the AUM breakdown is given in the above graph.

Northern Trust observes that “the relative importance of priorities is consistent across regions.”

Speaking of regions: the geography of the survey was heavily weighted toward the Americas. Eighty five percent of the investors questioned hailed from there (versus 11% from EMEA and 5% from APAC). The weighting wasn’t quite so drastic in the case of the managers included. Still, more than 60% of the managers hailed form the Americas (versus 21% APAC, and less than 20% for EMEA).

Transparency

It is on the matter of transparency that there is a large and perhaps troubling divergence between investors and managers.

A very lopsided majority of managers (90%) report that all or nearly all of their investors are satisfied with the level of transparency they’re getting.

But those investors don’t see it that way. A little more than half (55%) of investors say they want higher levels of transparency than they’re currently getting.

What Is On Offer (Percentages)

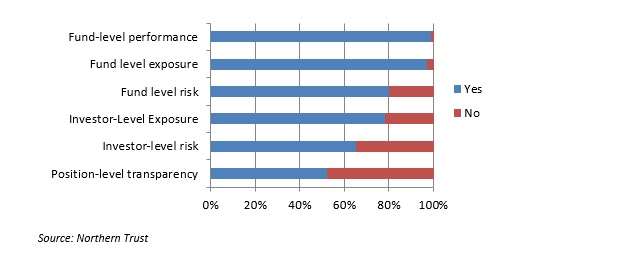

The word “transparency” has a number of different meanings. This may explain the gap between what managers think they’ve offered and what investors report they’re receiving. Northern Trust lists six of the meanings of the term and tells us how frequently each is offered by the managers surveyed. Fund level and fund exposure are both almost universally on offer, as the above table indicates. Other sorts of transparency … not so much.

Somewhat less than two-thirds of the managers offer investor level risk information (for example, investor-specific VaRs.) Fewer still offer position-level transparency.

A related question though is this: are the investors who want more transparency willing to pay to get it? And, if so, how much?

Investors in North America are sharply split on whether they would accept a 1 to 3 basis point increase in management fees in exchange for more transparency: a little less than 45% say “yes,” a little more than 55% say “no.” In both EMEA and APAC the division is close to 1/3d “yes” and 2/3s “no.”

Northern Trust is a Chicago based global financial services firm which was founded by Byron Laflin Smith back in 1889. As of the end of last year, it had assets under custody of $6 trillion, and assets under management of $934 billion.