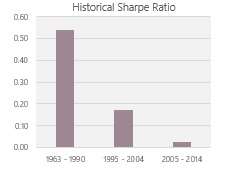

By Andrew Beer Of course it’s true until everyone knows it’s true. Famous economist in response to publication of Stocks for the Long Run (1994) Everyone likes bargains. Perhaps this explains the irresistible appeal of the Value benchmark factor. The original paper by Eugene Fama and Kenneth French in 1992 propagated the model that investors chase the latest highfliers, while boring “value” stocks are overlooked and underpriced. The key conclusion was that “value” stocks, as defined by low price-to-book ratios, outperform high multiple stocks and that this outperformance tends to be more pronounced during market downturns – a highly valuable property for an investment portfolio. But what if it’s all wrong? Not that the original paper was wrong, but that the return “anomaly” has been priced away or fundamentally changed? A simple review of risk adjusted returns highlights the issue. In 1963-90, the period studied, the Value factor had a Sharpe ratio of 0.54 – around double that of traditional assets over time. Since its “discovery,” the Sharpe ratio declined to 0.17 in 1995-2004 and dropped further to 0.03 in the past decade.[1]

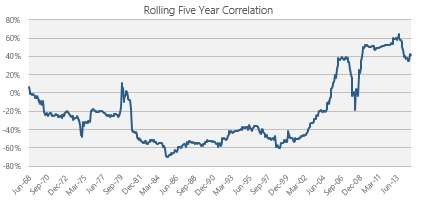

By Andrew Beer Of course it’s true until everyone knows it’s true. Famous economist in response to publication of Stocks for the Long Run (1994) Everyone likes bargains. Perhaps this explains the irresistible appeal of the Value benchmark factor. The original paper by Eugene Fama and Kenneth French in 1992 propagated the model that investors chase the latest highfliers, while boring “value” stocks are overlooked and underpriced. The key conclusion was that “value” stocks, as defined by low price-to-book ratios, outperform high multiple stocks and that this outperformance tends to be more pronounced during market downturns – a highly valuable property for an investment portfolio. But what if it’s all wrong? Not that the original paper was wrong, but that the return “anomaly” has been priced away or fundamentally changed? A simple review of risk adjusted returns highlights the issue. In 1963-90, the period studied, the Value factor had a Sharpe ratio of 0.54 – around double that of traditional assets over time. Since its “discovery,” the Sharpe ratio declined to 0.17 in 1995-2004 and dropped further to 0.03 in the past decade.[1]  What might this tell us? Most likely, excess returns were arbitraged away as more investors flocked to the space. Today, “value” investing is the norm rather than the anomaly, like when Warren Buffett ran a partnership in the 1960s and was buying “cigar butts” for less than net cash. The growth stock mantra of Peter Lynch and the idea of chasing “ten baggers” seems like a distant memory. Today, a quick screen on Bloomberg lists 942 value-focused equity mutual funds with assets under management of approximately $1.5 trillion. Add institutional managed accounts and value-focused investors like hedge funds and the number is much, much higher. Value isn’t overlooked anymore. What seems obvious is that the process of identifying and buying stocks is very different today. Imagine a typical investor in the 1970s. He reads the Wall Street Journal, scans the stock pages and calls his broker. The broker recommends an exciting growth stock with a great story, which maximizes his chance of getting paid a commission. It’s hard to see the same broker trying to explain, say, how a failing consolidated steel company is a bargain because the market’s overestimating the cost of pension liabilities. The oft touted growth bias of the typical investor, then, may be explained instead by agency issues with the advisor which are less relevant in a world with better dissemination of information, the shift to fee-based advisory and other tectonic shifts in the investing landscape. Another question is whether the composition of “cheap” stocks has changed over time. One possible hint comes from the correlation of the Value factor to the overall market. Correlation was decidedly negative in the period studied and the subsequent decade, which bolstered the argument that cheap stocks were “safer”: they fell less when markets declined, and vice versa. Over past decade, however, the correlation has been clearly positive. This is harder to explain and undercuts the argument for Value as a diversifier under Modern Portfolio Theory.[2] What’s changed? One possibility is industry or sector bias. Unfortunately, it’s difficult to tell given the inaccuracy of simple classifications like SIC codes, especially given how much US industry has changed over the past decades (e.g. deconglomerization). Another possibility is a change in accounting standards – for instance, the elimination of pooling of interests acquisitions under GAAP in 2001. Did this fundamentally alter the concept of “book value”?

What might this tell us? Most likely, excess returns were arbitraged away as more investors flocked to the space. Today, “value” investing is the norm rather than the anomaly, like when Warren Buffett ran a partnership in the 1960s and was buying “cigar butts” for less than net cash. The growth stock mantra of Peter Lynch and the idea of chasing “ten baggers” seems like a distant memory. Today, a quick screen on Bloomberg lists 942 value-focused equity mutual funds with assets under management of approximately $1.5 trillion. Add institutional managed accounts and value-focused investors like hedge funds and the number is much, much higher. Value isn’t overlooked anymore. What seems obvious is that the process of identifying and buying stocks is very different today. Imagine a typical investor in the 1970s. He reads the Wall Street Journal, scans the stock pages and calls his broker. The broker recommends an exciting growth stock with a great story, which maximizes his chance of getting paid a commission. It’s hard to see the same broker trying to explain, say, how a failing consolidated steel company is a bargain because the market’s overestimating the cost of pension liabilities. The oft touted growth bias of the typical investor, then, may be explained instead by agency issues with the advisor which are less relevant in a world with better dissemination of information, the shift to fee-based advisory and other tectonic shifts in the investing landscape. Another question is whether the composition of “cheap” stocks has changed over time. One possible hint comes from the correlation of the Value factor to the overall market. Correlation was decidedly negative in the period studied and the subsequent decade, which bolstered the argument that cheap stocks were “safer”: they fell less when markets declined, and vice versa. Over past decade, however, the correlation has been clearly positive. This is harder to explain and undercuts the argument for Value as a diversifier under Modern Portfolio Theory.[2] What’s changed? One possibility is industry or sector bias. Unfortunately, it’s difficult to tell given the inaccuracy of simple classifications like SIC codes, especially given how much US industry has changed over the past decades (e.g. deconglomerization). Another possibility is a change in accounting standards – for instance, the elimination of pooling of interests acquisitions under GAAP in 2001. Did this fundamentally alter the concept of “book value”?  The danger of investing based on academic studies is that our own biases often rise to the surface. We tend to overlook the fact that published studies invariably have “interesting” results – the pressure to data mine should not be underestimated. What looks good on paper may have little relevance once translated into an investment strategy – a failure to screen for market capitalization, for example, can undercut the notion of “investability.” Conclusions are emphasized over assumptions; yet, the latter are equally, if not more, important. We often hope that such studies reveal an immutable truism about the market and investors – since relying on truisms is easier than messy realities. When studies like the HML paper become canonical – what investing course doesn’t cover the Fama-French factors? – we cling to the original conclusions even as the world evolves. The end result is that academic studies can steer investors to strategies that might have worked decades ago, but not today. The performance of the Value factor “post-discovery” should be a cautionary tale for investors considering the panoply of smart beta and alternative risk premia today. [1]Based on data available on Kenneth French’s data library. [2] Market returns from Kenneth French’s data library were utilized. Andrew Beer, CEO: At Beachhead, Mr. Beer oversees all marketing and research efforts and is influential in portfolio construction. Mr. Beer began his career in mergers & acquisitions at the James D. Wolfensohn Company, a boutique firm founded by the forthcoming President of the World Bank. Mr. Beer worked in leveraged buyouts at the Thomas H. Lee Company in Boston during his tenure at Harvard Business School. Upon graduating, he joined the Baupost Group, a leading hedge fund firm, as one of six investment professionals. Additionally, Mr. Beer co-founded Pinnacle Asset Management (leading commodity fund) and Apex Capital Management (Greater China hedge fund). Mr. Beer is an active member of the Board of Directors of the US Fund for UNICEF, where he serves as Chairman of the Bridge Fund, an innovative financing vehicle designed to accelerate the worldwide delivery of life-saving goods to children in need. With his wife, Mr. Beer is a co-founder of the Pierrepont School, a co-educational K-12 independent school located in Westport, CT. Mr. Beer received his Master in Business Administration degree as a Baker Scholar from Harvard Business School, and his Bachelor of Arts degree, magna cum laude, from Harvard College.

The danger of investing based on academic studies is that our own biases often rise to the surface. We tend to overlook the fact that published studies invariably have “interesting” results – the pressure to data mine should not be underestimated. What looks good on paper may have little relevance once translated into an investment strategy – a failure to screen for market capitalization, for example, can undercut the notion of “investability.” Conclusions are emphasized over assumptions; yet, the latter are equally, if not more, important. We often hope that such studies reveal an immutable truism about the market and investors – since relying on truisms is easier than messy realities. When studies like the HML paper become canonical – what investing course doesn’t cover the Fama-French factors? – we cling to the original conclusions even as the world evolves. The end result is that academic studies can steer investors to strategies that might have worked decades ago, but not today. The performance of the Value factor “post-discovery” should be a cautionary tale for investors considering the panoply of smart beta and alternative risk premia today. [1]Based on data available on Kenneth French’s data library. [2] Market returns from Kenneth French’s data library were utilized. Andrew Beer, CEO: At Beachhead, Mr. Beer oversees all marketing and research efforts and is influential in portfolio construction. Mr. Beer began his career in mergers & acquisitions at the James D. Wolfensohn Company, a boutique firm founded by the forthcoming President of the World Bank. Mr. Beer worked in leveraged buyouts at the Thomas H. Lee Company in Boston during his tenure at Harvard Business School. Upon graduating, he joined the Baupost Group, a leading hedge fund firm, as one of six investment professionals. Additionally, Mr. Beer co-founded Pinnacle Asset Management (leading commodity fund) and Apex Capital Management (Greater China hedge fund). Mr. Beer is an active member of the Board of Directors of the US Fund for UNICEF, where he serves as Chairman of the Bridge Fund, an innovative financing vehicle designed to accelerate the worldwide delivery of life-saving goods to children in need. With his wife, Mr. Beer is a co-founder of the Pierrepont School, a co-educational K-12 independent school located in Westport, CT. Mr. Beer received his Master in Business Administration degree as a Baker Scholar from Harvard Business School, and his Bachelor of Arts degree, magna cum laude, from Harvard College.

Search

Search Close

Close