TABB ran a piece recently by their contributing analyst, Rebecca Healey, on the elusiveness of the “natural block.”

TABB ran a piece recently by their contributing analyst, Rebecca Healey, on the elusiveness of the “natural block.”

Ms Healey knows of what she speaks. At Credit Suisse, she played a key role in launching a successful Advanced Execution Services product to hedge funds. She was also employed by the British Embassy in Bahrain from 2008 to 2010, where she launched the UK government’s financial services strategy.

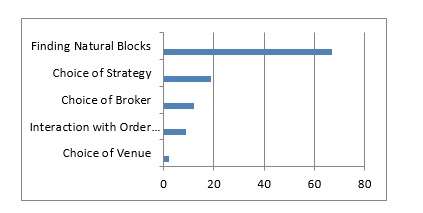

Presumably by trading in “natural blocks” she doesn’t mean anything especially Edenic: block trading in the wilderness, or amongst traders au naturel. She simply refers to trading on blocks without excessive execution risk and in a way that can avoid market impact. This, she says, is an elusive goal. The above chart, adapted from Fig. 1 in her paper, indicates how desirable that goal is. Two thirds of buy side participants say that a move to natural blocks is their most important factor in terms of execution.

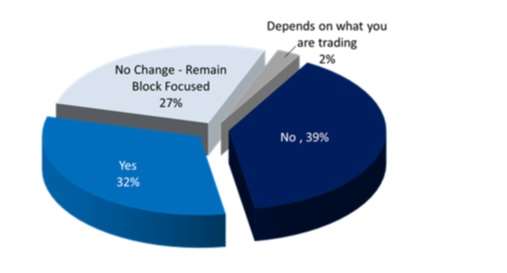

Yet how many are actually doing it? Not so much.

Source, TABBGroup, Fig. 2

Less than one third say simply “yes,” they are moving away from schedule based trading back to blocks.

Sin and Repentance

Recent regulatory and technological changes have made block trading difficult. For example, regulators now require that firms, both on the buy and on the sell side, establish that they are offering “best execution.” In satisfying regulatory demands to this effect, firms will respond to order imbalances or times of high market momentum by trading in smaller sizes.

“As market volatility increases,” Healey writes, “buy-side firms will need to capitalize on opportunities as and when they become available.”

One positive sign for those who want to get back to the natural blocks is the Large-in-Scale waiver in Europe. The LiS waiver works to alleviate the double volume cap mechanism within the European Market Abuse Regulation (MAR). Indeed, an unnamed “large UK asset manager” told TABB, “We all know the caps are ridiculous but hopefully it will focus people on stocking to the LIS waiver.”

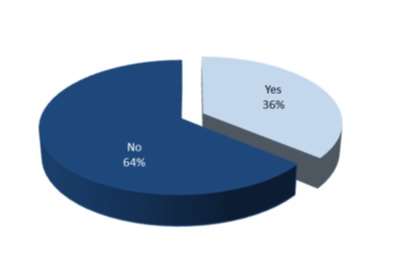

Despite their initial purpose, the existence of these caps may not do much to limit use of dark pools. The pie below indicates the answers to the question whether a volume cap will “impact your usage of dark pools.”

Source: TABB Group, Fig. 9

Markets are highly adaptive institutions and the buy-side will find ways to trade in ways that it finds most effective. Meanwhile if the caps are a regulatory sin, LiS may serve as repentance, and back to the garden we head, right? But this leaves some fascinating questions about the hows.

In particular: if a return to natural blocks does take place, will brokers have a place in developing solutions, or will natural blocks develop through direct buy-side to buy-side negotiation? That depends on how much or little brokers add to the flow of information. The buy side has to be able to rely on Indications of Interest (IoIs), which are now sometimes darkly re-christened “lie on lies.”

Indeed, increasing dependence on IoIs has found a regulatory echo in the inclusion of false IoIs as manipulative behavior under MAR.

Meanwhile, exchanges are introducing new services that offer the buy side new ways of trading blocks. Healey references initiatives from the LSE, BATS, Cho-X, and Luminex. BATS will offer continuous auctions operating within a European Best Bid and Offer (EBBO) collar. These auctions will last “from between 100 millisecond to five minutes, depending on demand and market capitalization of the company.” The goal is to prevent information leakage, although as Healey observes, success here will depend “on whether the whole size of the order can be executed.”

The LSE and NYSE are also going to increase the availability of auctions, although they won’t be continuously triggered throughout the day, they’ll be offered at specified times and via the main order books.

A Commenter

When an abstract of the Healey paper appeared on the Tabb Forum, a commenter, who identified himself as someone who “trades blocks whenever I can,” in contrast to others who (on his account) just say “they would prefer to trade blocks,” expressed some views that repay attention. They may represent a good deal of sentiment among participants.

He said that the sell side is very far behind on “understanding what it takes to shop and negotiate a block,” while the buy side has become very risk averse. In connection with that risk aversion, he says, the buy side has become paranoid about transaction costs analysis (TCA) reporting. He concludes that improvements require the buy side to abandon the “goal of benchmarking to whatever TCA crap they benchmark to.”

Words to live by.