The British Private Equity & Venture Capital Association, in a new paper, contends that private equity has a valuable part to play in the portfolios of defined contribution schemes, for the simple reason that the PE world offers high returns in an era of low interest rates.

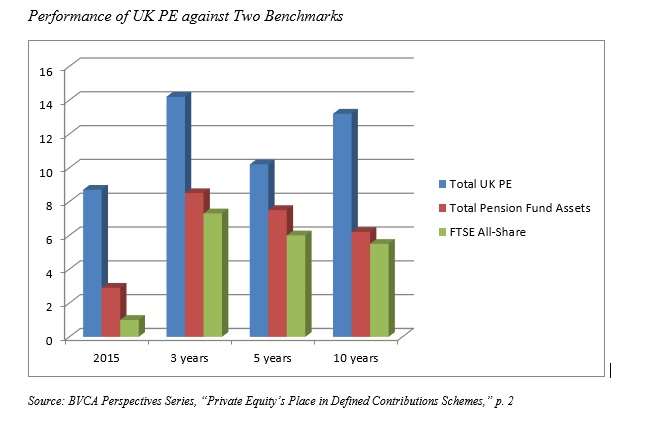

To make that point, in the British context especially, it offers the table adapted below, indicating that total UK private equity has beaten the FTSE all-share by a wide margin in any of the four time frames suggested, from a single year to a decade-long period.

The asset class, then, “continues to produce robust and consistent returns, even during times of recession and economic downturn.” The ten-year period on the right hand side of the above table obviously takes in the global financial crises of 2007-09.

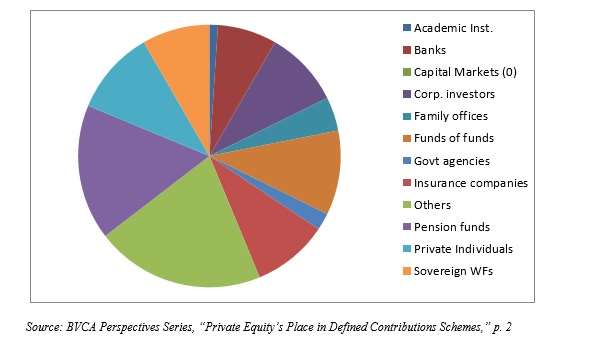

Due to the clearly desirable features of the PE asset class, and pensioners’ need of those features: more than one-seventh of the capital raised by UK PE finds came from pension funds in 2015.

But a shift has long been underway, in the United Kingdom as in much of the rest of the world, away from defined benefit plans and toward defined contributions plans. This movement, as the BVCA says, “raises fundamental questions about the nature of returns within the pensions industry.” To the younger employees in the workforce, DB is often nowadays simply unavailable. So … do DC plans allow the workers to avail themselves of the same opportunities, making use of the resource offered by the performance of the PE industry?

UK Private Equity Fund Capital Sources: 2015

As an issue for general partners in the PE world, BVCA thinks the answer must be affirmative. The GPs must make their services available to the DC investors as DB’s role in the economy declines.

“This shift [to DC] may not be a concern for GPs over this or the next fundraising cycle but it raises some obvious questions around what happens for the next generation and whether the private equity industry should take notice.”

Default Options and Sponsors

Fortunately (for GPs), as money has flowed into the DC space, sponsors have adopted “default investment options for their participants in order to help them manage the risks associated with long-term investment.” So the GPs don’t have to make a pitch to each individual worker/investor. They can make their pitch to those sponsors for a place in the default options.

As experience in the US has shown, “these default options can be very large and highly customized to meet the specific needs of the sponsor’s workforce.”

But there is a cultural problem. In order to make their appeal to sponsors, PE funds will have to change their attitude toward time. Under their ‘normal’ circumstances, PE managers take months to actually start investing money committed to their care, and the committed capital might not be fully drawn until five years have passed. But the culture of the DC space is one of putting money to work quickly.

Also, relatedly, that notorious “J” curve in PE returns is a barrier to widespread adoption of this asset class in the DC world.

This is where secondaries play a critical role. Secondary PE investments can create a smoother and earlier stream of returns than a more direct approach to the field can.

Valuation

Another consideration is the frequency of valuation. Public equities of course on the one hand have their values set by the market and the prices are printed in the daily newspapers. GPs on the other hand “typically provide valuation updates on their funds … to investors on a quarterly basis or even every six months.” DC investors and their sponsors will want daily valuations and the BVCA advises GPs just to provide this, get used to it already. To provide such valuations, they need to “have a thorough understanding of the fair market valuation techniques used by the managers of their portfolio companies,” then consider “specific changes in company values” and the broader economy, and make estimates accordingly.

In general, the BVCA expects that the barriers can be overcome and a happy marriage between PE GPs on the one hand and DC sponsors on the other can be arranged though this will require some creativity and some patience.