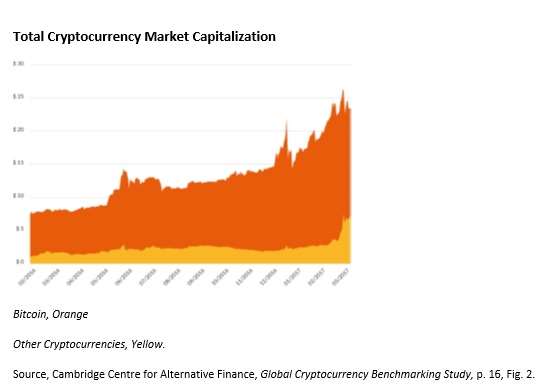

It is clear by now to even the most hardened skeptic that cryptocurrency, the class of assets of which bitcoin is the paradigm, is much more than a passing fad. Yes, the field may once have been too closely associated with survivalists, cranks, and bit players in the story of the founding of Facebook, but as of April 2017, by which time the combined market value of all such currencies was $27 billion, writing off the whole field looked very much like a form of blindness. It isn’t merely that $27 billion is an impressive big number (though it is). It is that along the way to this size, the industry has generated new ways of doing business and thinking about doing business which are in turn proving themselves. Cryptocurrency isn’t a fad: it’s an ecosystem. Accordingly, a little more than nine years after the publication of the landmark paper by Satoshi Nakamoto, Cambridge Centre for Alternative Finance has issued its “first global cryptocurrency benchmarking study.” It offers the public “an empirical picture of the current state of this still maturing industry.” The graph below illustrates the dramatic growth of the industry in little more than one year, from February 2016 through March 2017.  Bitcoin retains its dominance, though there are significant challengers included in the yellow space at the bottom of that graph. The most important of these challengers is Ether (ETH), “the native cryptocurrency of the Ethereum network,” as the Centre’s report says. Ninety-eight percent of the “participating exchanges, wallets, and payment companies” surveyed supported bitcoin. Ether came in a distant second place by that metric, at 33%. Litecoin (LTC) came in third, at 26%. Some key points in the report concern the exchanges sector of the industry. This sector has the highest number of operating entities in the broader industry and the highest employment numbers. It also shows significant geographical dispersion.

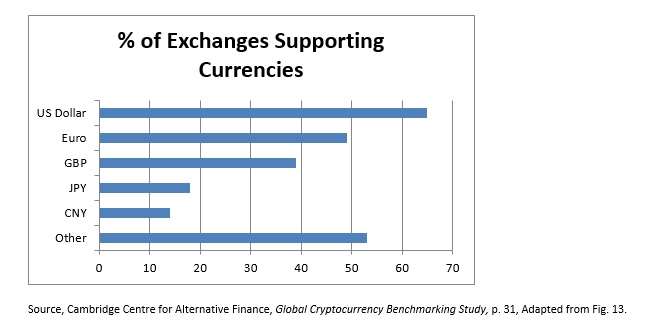

Bitcoin retains its dominance, though there are significant challengers included in the yellow space at the bottom of that graph. The most important of these challengers is Ether (ETH), “the native cryptocurrency of the Ethereum network,” as the Centre’s report says. Ninety-eight percent of the “participating exchanges, wallets, and payment companies” surveyed supported bitcoin. Ether came in a distant second place by that metric, at 33%. Litecoin (LTC) came in third, at 26%. Some key points in the report concern the exchanges sector of the industry. This sector has the highest number of operating entities in the broader industry and the highest employment numbers. It also shows significant geographical dispersion.  As to that dispersion, the authors of this study collected data from 51 exchanges in 27 countries. They observe that the countries include “all world regions.” Europe has the largest sheer number of exchanges followed by the Asia-Pacific area: but North America, Latin America, the Middle East and Africa – all have exchanges. Large and Small Exchanges The likelihood that a cryptocurrency exchange will “hold a formal government license” is inversely related to its size. The smaller are licensed entities, the larger tend not to be. In geographical terms, the Asia-Pacific region has upheld its reputation for laissez-faire. Eighty-five percent of cryptocurrency exchanges in that region have no license. On the other hand, a full 78% of exchanges in North America have “a formal government license or authorization.” The study also looked into the distribution of the (traditional) currencies supported by the cryptocurrency exchanges. The graph above illustrates the result of that inquiry. The U.S. dollar is dominant, and the “other” figure is high because many small exchanges “service local markets and make cryptocurrencies more available in many countries,” they naturally specialize in their local currencies. There have been scandals and failures among the centralized exchanges, and a priori one might have expected those events to generate an exodus to peer-to-peer exchanges. Yet there has been no such exodus. Only 2 of the 51 exchanges surveyed might be described as P2P. One of the problems with running a small cryptocurrency exchange is that it can be difficult to obtain or maintain banking relationships. Larger exchanges “have this risk factor under control,” the report says. Wallets and Miners The humbly named “wallets” for such currencies are also a critical part of the ecosystem, and a focus of the report. It observes that they have “evolved from simple software programs … to sophisticated applications that offer a variety of technical features and additional services that go beyond the simple storage of cryptocurrency.” More than four fifths of wallet providers (81%) are based either in North America or in Europe, which seems high since on 61% of wallet users are in one of those two areas. Finally, in their concluding observation, the authors of the report say that they expect that as block awards decrease the cryptocurrency miners will have to use innovative economic incentives “in order to continue providing hashing power to secure the system,” powering a new security-driven direction in its evolution.

As to that dispersion, the authors of this study collected data from 51 exchanges in 27 countries. They observe that the countries include “all world regions.” Europe has the largest sheer number of exchanges followed by the Asia-Pacific area: but North America, Latin America, the Middle East and Africa – all have exchanges. Large and Small Exchanges The likelihood that a cryptocurrency exchange will “hold a formal government license” is inversely related to its size. The smaller are licensed entities, the larger tend not to be. In geographical terms, the Asia-Pacific region has upheld its reputation for laissez-faire. Eighty-five percent of cryptocurrency exchanges in that region have no license. On the other hand, a full 78% of exchanges in North America have “a formal government license or authorization.” The study also looked into the distribution of the (traditional) currencies supported by the cryptocurrency exchanges. The graph above illustrates the result of that inquiry. The U.S. dollar is dominant, and the “other” figure is high because many small exchanges “service local markets and make cryptocurrencies more available in many countries,” they naturally specialize in their local currencies. There have been scandals and failures among the centralized exchanges, and a priori one might have expected those events to generate an exodus to peer-to-peer exchanges. Yet there has been no such exodus. Only 2 of the 51 exchanges surveyed might be described as P2P. One of the problems with running a small cryptocurrency exchange is that it can be difficult to obtain or maintain banking relationships. Larger exchanges “have this risk factor under control,” the report says. Wallets and Miners The humbly named “wallets” for such currencies are also a critical part of the ecosystem, and a focus of the report. It observes that they have “evolved from simple software programs … to sophisticated applications that offer a variety of technical features and additional services that go beyond the simple storage of cryptocurrency.” More than four fifths of wallet providers (81%) are based either in North America or in Europe, which seems high since on 61% of wallet users are in one of those two areas. Finally, in their concluding observation, the authors of the report say that they expect that as block awards decrease the cryptocurrency miners will have to use innovative economic incentives “in order to continue providing hashing power to secure the system,” powering a new security-driven direction in its evolution.

Search

Search Close

Close