By Christian H. Mueller-Glissmann, Global Investment Research, at Goldman Sachs.

At a time when stocks are sliding, it can be hard (and painful) to remember that equities have the best chance of getting investors an attractive return over the longer term. Portfolios have gotten riskier since the beginning of the year, as bonds and stocks have fallen together. But there are ways investors can insulate portfolios until the turbulence subsides, according to Goldman Sachs Research.

“We’re looking at strategies that reduce risk without just going into cash — that allow you to stay invested,” says Christian Mueller-Glissmann, head of asset allocation research within portfolio strategy at Goldman Sachs. He says there are five strategies investors can use to avoid trying to time the market and getting hit with losses by taking more investment risk too early in a bear market or missing out on gains by being too late. They can be used with a range of portfolios, from balanced (a mix of stocks and bonds) portfolios to ones that are loaded up on stocks.

These strategies aim to optimize the trade-off between risk reduction and cost. A wide spectrum of investors, from individuals to large institutions, can use many of these tactics. “Volatility might linger,” he says. “We’re trying to minimize the cost so you can potentially implement these strategies for a few months.”

Go up in quality. That can mean buying stocks and bonds of companies with strong balance sheets, steady profits and dividends, or those that are less volatile. Whereas investors were rewarded in the last cycle for buying into companies with the potential for high growth in the future, stocks with proven business models and pricing power that pay dividends can offer some protection in a bear market, Mueller-Glissmann says.

That idea also applies to foreign exchange, with the U.S. currency an example of a high-quality asset. “With the dollar, here you have a central bank that’s fighting inflation very aggressively, very credibly, and it’s a reserve currency,” Mueller-Glissmann says. “The dollar has already appreciated strongly, and we feel there’s potentially more to go.”

Currency trades are a type of relative-value investing — positioning for one asset to increase in price while another declines — which Mueller-Glissmann says is likely to be more important in this cycle. That’s a switch from recent decades, when huge swaths of assets were swept up in an enormous bull market giving passive investments a boost. Picking individual stocks and bonds, instead of buying the broad index, is poised to become more valuable to investors going forward, he says.

Hedge funds are providing more of a hedge. It was difficult for these asset managers to beat a long-only benchmark index in the last cycle when just about everything was rallying, Mueller-Glissmann says. When there was a scarcity of growth and fears of economic stagnation, central banks routinely stepped in to make financing cheaper and easier, which tended to raise asset prices across markets.

Now with a spike in inflation, the reverse is happening — central banks can’t buffer the stock market when it falls. These days the likes of the U.S. Federal Reserve are actively trying to tighten financial conditions, reduce wage and price increases and rebalance the job market. “In the last cycle, central banks were your risk manager,” Mueller-Glissmann says. “Now they are actually driving the risks via higher inflation-adjusted yields and capping the upside in some markets.”

That could be a boost for some key strategies that hedge funds use (in particular trend-following). While broad hedge fund returns lagged behind a simple 60-40 portfolio of stocks and bonds after the financial crisis in 2008, hedge funds beat the 60-40 in the early 1990s and the beginning of this century, particularly during bear markets, according to Goldman Sachs Research. Some hedge funds are publicly listed on the stock market, and some widely available exchange-traded funds are linked to these methods.

Strategies that vary a portfolio’s risk depending on market volatility — known as dynamic risk allocation — may also be an opportunity. Some ETFs have dynamic-risk strategies.

“It’s a simple idea: If things are volatile, you probably want to take a bit less risk,” Mueller-Glissmann says. “It’s sending me a signal that we are in a riskier environment and that probably means I need to own a bit less equity. This type of rule has, in the very long run, worked remarkably well.”

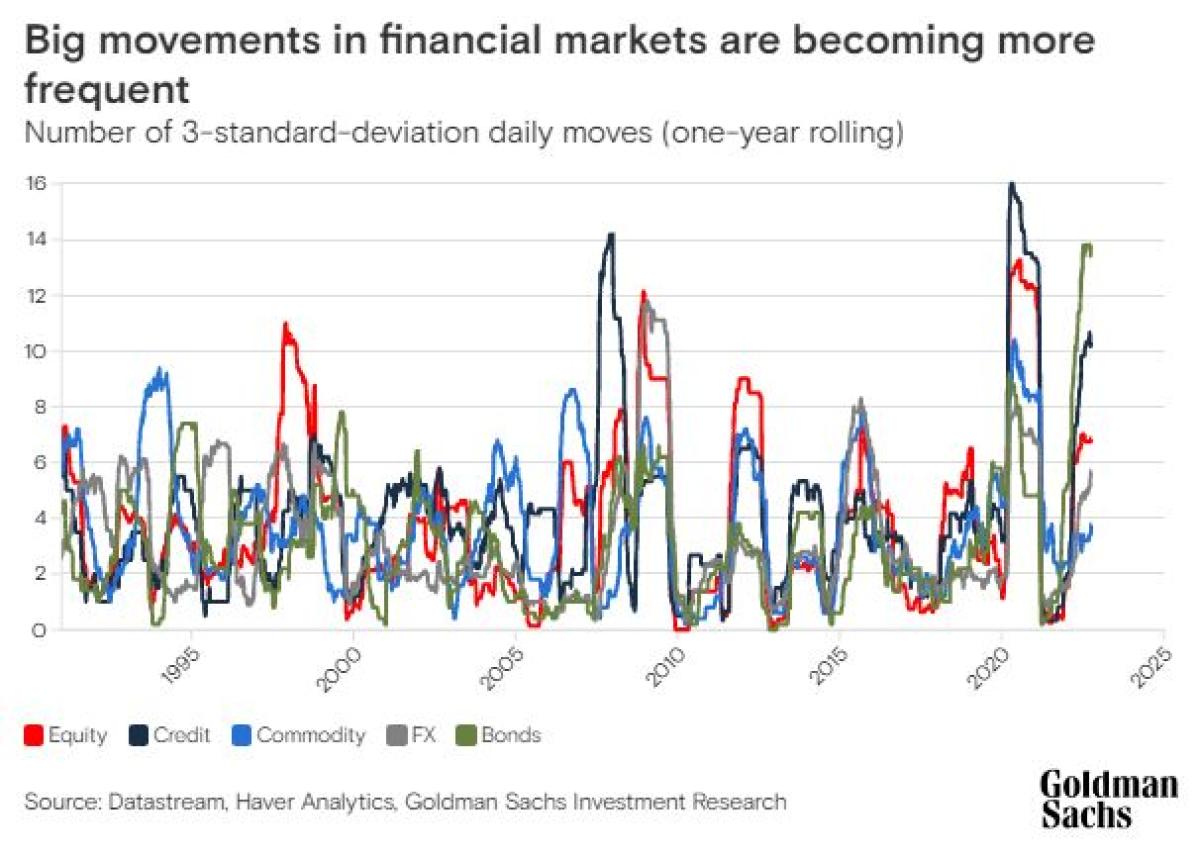

Investors can use options to directly hedge their portfolios against a drop in prices. But this tactic becomes costly over time: Negative carry, where investments cost more than they return, piles up if this strategy is used for longer periods, and prices often need to move substantially for options contracts to pay out. But market moves that are much larger than you’d normally expect — known as tail events— are becoming more common as central banks retreat from supporting financial markets. That means options contracts could pay out more often.

“We’re entering a world with higher inflation, where cycles might become shorter, volatility might become higher and by extension, you have the ability to generate more frequent tail events,” Mueller-Glissmann says. “Maybe they won’t be as extreme as during and since the global financial crisis. The probability or the likelihood of an option hedge paying off is higher but the payoff might be lower — but that will still make them more useful.”

This tactic can be used in cross-asset strategies as well: financial markets tend to become more correlated during a bear market in stocks, and currencies and commodities in particular tend to have larger swings in prices during periods of higher inflation, meaning a higher likelihood of a pay-out from options linked to those assets. Call options on the U.S. dollar (which pay if the greenback rallies) were also a useful strategy this year, as were put options on bonds (which pay if fixed-income prices decline).

The shift in central bank policies can, again, be important here. It was difficult to profit from large drops in financial markets after the credit crisis because policymakers essentially put on a floor under those declines. The opposite is happening now, and that can make it more attractive to sell call options (bets that an asset will increase in price) or to buy puts (bets that an asset will decline in price), known as so-called collaring strategies.

“It’s again one of those strategies which in the past used to be very popular,” Mueller-Glissmann says. “You need to come back to old rules, like volatility targeting and momentum investing. It’s essentially a step back to what worked in past.”

“There’s a bit of a renaissance of risk management full stop,” he added.

Click here for more Goldman Sachs Insights

About the Author:

Christian H. Mueller-Glissmann heads asset allocation research within portfolio strategy. He also writes research on derivatives with a focus on dividends, volatility and correlation.

Christian is a member of the Structured Research Products Working Group. He is also a trustee of the firm’s UK Defined Benefit Pension Scheme and member of its investment committee. Previously, he worked on the Tactical Research Group, focused on quantitative investment strategies. Prior to that, Christian worked in derivatives trading in Frankfurt. He joined Goldman Sachs in 2005 as an analyst and was named managing director in 2015. Christian earned a master's degree in Finance and Management from the University of Mannheim. He also studied at Warwick Business School and ESSEC Business School. Christian is a CFA charter holder.