By Steve Richey, co-CIO, Head of Convexity Alpha, and Scott Maidel, CFA, Head of Business Development at QVR Advisors.

Derivatives markets are about supply and demand. These are markets where risk is manufactured for the end user. End users dominate the market and are the marginal price setters. Some are more sophisticated than others but are generally concerned about first-order objectives, such as directional exposure, a specific trade for a systematic strategy, or any sort of product-based price-insensitive trading. When themes within end-user flows grow excessively relative to the size of the market, they significantly affect market prices and change risk premia. For long-time readers, these statements should sound familiar. This is what we see today with the oversupply of option-selling strategies. These product-based price-insensitive strategies have a material effect on implied volatility and therefore the pricing of options. We view this end-user group as causing a large structural dislocation.

How did this happen? What shifted in markets for this to occur?

Post Global Financial Crisis (“GFC”), both retail and institutional demand for option-selling strategies started to grow rapidly. Large groups of investors are now viewing it as an “evergreen” asset class for income generation. During the few years proceeding GFC, many consultants started to write papers extolling the benefits of short volatility strategies as defensive equity and lower volatility equity substitutes. Ex-post then prior decades there was much data which shows this was true. Ex-ante, this turned out to be false. This is especially true when it has been a while since the last crisis and tail risk sellers are emboldened.

An accurate description of benchmarks such as the Cboe BXM or PUT Indexes historically would be “Equity-like returns with lower volatility”, but today should be replaced with the statement, “Equity-like risk with lower returns”. As with all risk premiums, the attractiveness ebbs and flows. Pre-GFC, short-term options tended to be expensive. As a result, harvesting a volatility risk premium was attractive and back-tested well. We have said before, in quantitative equity strategies, one can argue ad nauseam about the statistical evidence via which one estimates ex-post whether there was a risk premium. In derivatives markets, you can simply look at the price.

What do we see today? How are asset allocators allocating to volatility strategies?

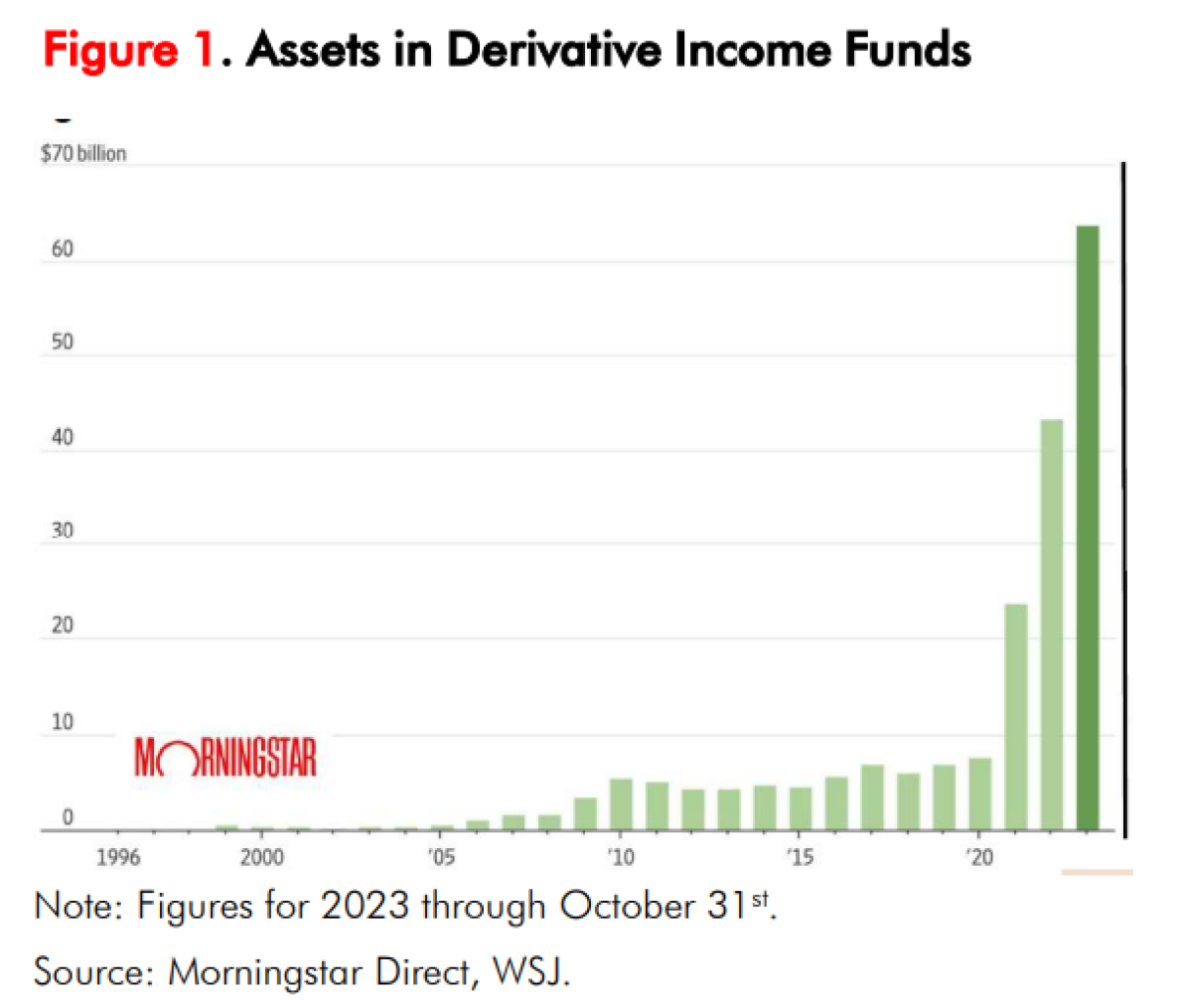

As with traditional asset classes or alternatives as well (ie CTAs, Volatility, etc.), it is reasonable to attempt to cleanly dissect into various strategy categories whether by asset or theme. In the volatility hedge fund space, this is usually done as either Tail Hedging, Long Volatility, Short Volatility, or Market Neutral. In general derivatives strategy, Hedged Equity, and Covered Calls (aka Volatility Risk Premium “VRP”) have historically been the most prevalent and widely used strategies. And in fact, have exploded in popularity in recent years, see Figure 1, from creative marketing spin.

For this paper, we will highlight the recurring questions we receive about short volatility strategies from our vantage points as a Derivatives-based hedge fund manager. For more on the history of the derivatives markets from a relative value volatility arbitrage manager perspective, pointing out the risks and opportunities that each cycle has brought please see our Evolution of Derivatives Markets And Arbitrage paper Q3 2023.

COMMON SHORT VOLATILITY DISCUSSIONS: FACT OR FICTION

First, what are we seeing today?

- Option selling for “income”, premium is yield, right?

- Options are on average overpriced, the VRP right? So why not sell them systematically?

- What about options-based equity replacement strategies? Also known as defensive equity programs?

OPTION SELLING FOR “INCOME”

A very common story we hear is: “Covered call selling uses an investor’s equity position to generate income. By selling a call worth 1% every month, for example, the investor adds a 12% yield.”

THIS IS FICTION

This is highly misleading. It is even too much for Morningstar historically, which felt to comment on it in 2013 (remember this date!) given the slew of option-selling mutual funds hitting the market. They have however given way to the option selling tsunami and created a Derivative Income Fund Category. Just like covered calls are not economically equivalent to leaving resting limit orders higher, to sell a stock, they are also not an “income generating” strategy that reliably benefits from choppy, range-bound market. Selling covered calls is a short volatility position that swings in the market over the expiration window or roll period; it will be more muted than implied ex-ante by the price of the options.

OPTIONS SELLING AS AN “INSURANCE PROVIDER”

One popular investment thesis that permeates call write and put write (aka defensive equity) pitches: “Options are systematically overpriced… instead of buying options, we prefer to overwrite calls or replace equity exposure with cash-secured puts to buffer downside risk and be the insurance provider.”

THIS IS FICTION

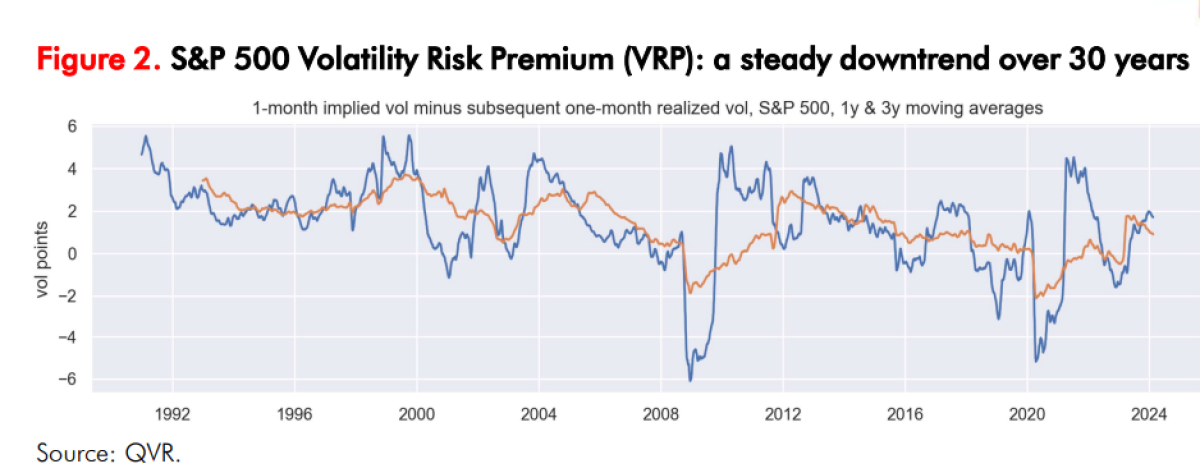

First is the question of the risk premium associated with options. There is good evidence that short-term options were relatively expensive for many years. This is reflected in the observed volatility risk premium (“VRP”) (1-month at the money implied volatility of S&P options, minus subsequent 1-month realized volatility). Figure 2 shows a trailing 3-year average.

The volatility risk premium was 2.5 points on average before 2006. There had been almost no risk premium at all on a trailing 3-year basis even before GFC and the March 2020 crash. That suggests the expected returns of option selling were likely negative on a forward-looking, probability-weighted basis by mid-2008 and by early 2020, because thin positive returns in the median scenario are more than offset by the possibility of a tail event.

Volatility selling has become increasingly popular over time, with large groups of market participants viewing itas an “evergreen” asset class for income generation, which is a misleading marketing-oriented spin. The point is that options are sometimes, but not always, expensive; and they have steadily become less expensive, even arguably fair to cheaply valued on average here over time.

OPTION SELLING FOR “DEFENSIVE EQUITY” OR “HEDGED EQUITY”

Some common views among asset consultants are: “Options are systematically overpriced… instead of buying tail hedges, we prefer to replace equity exposure with cash-secured puts or overwrite calls in order to buffer downside risk and reduce portfolio volatility.”

THIS IS FICTION

Two of the most common Cboe benchmark indices for option selling and hedged equity are:

- BXM: Cboe S&P 500 BuyWrite Index (aka Call overwriting)

- HFRXEH: HFRX Equity Hedge Index

The BXM is the most popular S&P 500 call overwriting benchmark simply selling 1-month ATM calls. Equity hedge strategies maintain both long and short positions in primarily equity and equity derivative securities. Some investment managers even use HFRXEH as a secondary benchmark.

Volatility selling strategies as equity replacement offer some path diversification, but not outright risk reduction in all types of paths. An option selling strategy is not inherently risk-reducing: a covered call or a cash secured put selling strategy has effectively the same exposure as outright equities in a sharp market selloff. Option selling strategies are short convexity, which means loses money at a faster rate the worse things get. As a result, while they may make money over time on a standalone basis, they are potentially less additive from an overall portfolio perspective to an already equity-heavy asset allocation.

So why do these short volatility strategies continue to be so popular even amongst institutional investors today?

REPACKAGE, REBRAND, REBENCHMARK

Over time, market participants generally accepted strategies such as the Cboe BXM index to be re-benchmarked from S&P 500 total return to a split between T-Bills and S&P 500 total return. This is misleading and represents an effort to lower the performance bar.

Another spin is to rebrand as a hedge fund substitute. We see this quite often with volatility selling strategies relative to the HFRXEH index. As the saying goes, this works until it doesn’t. During a period of low cash rates, the 50-50 split benchmark was clever and widely used but should rightfully encounter some pushback from allocators moving forward. The most recent 10-year period was primarily a strong upside equity period, which masks poor manager skill and necessitates minimizing large benchmark hurdles for managers.

A logical question here is, what is the effect of all this product growth on future returns?

IMPACT OF VOLATILITY SELLING PRODUCT GROWTH OF PREVALENT STRATEGIES

In the following section, we showcase a simple up-down capture study on two investable benchmarks.

Up capture measures return capture as a percent of monthly upside. A positive capture is ideal in upside (ie SPX+1%, strategy +0.5%, equates to a +50% up capture).

Down capture measures return capture as a percent of monthly downside. A positive capture figure is aligned withthe direction of asset downside (ie SPX -1%, strategy -0.5%, equates to a +50% down capture). o A negative capture however is ideal in downside (ie SPX –1%, strategy +0.5%, equates to -50% downcapture).

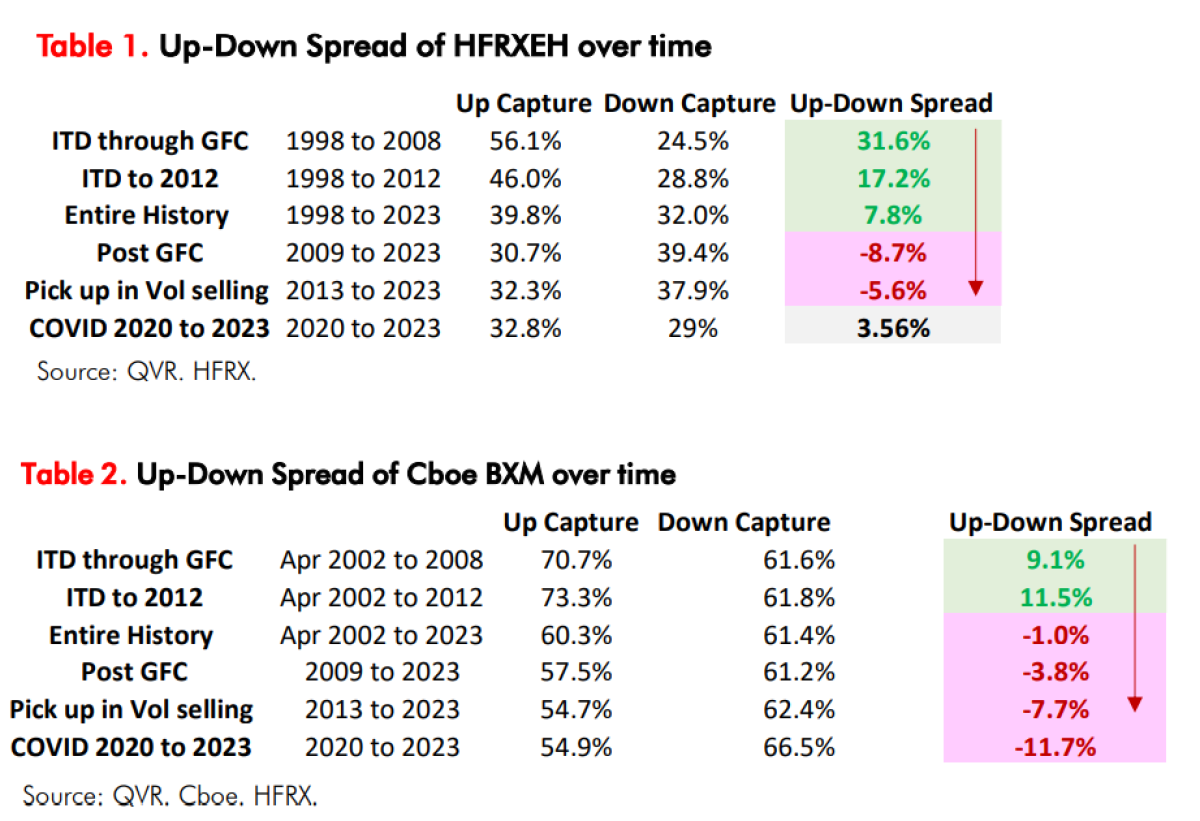

Up minus down spread is indicative of manager skill and future returns. Over time, we have seen a degradation of up-down capture for investable strategies such as the Cboe BXM and investable indexes such as the HFRXEH index. The oversupply of option-selling strategies has changed the game for many prevalent funds. This is a major problem for many investment managers. These product-based price-insensitive strategies have a material effect on implied volatility and therefore the pricing of options. These end-users are contributing to a large structural dislocation. This is unequivocally bad news for managers employing these types of strategies.

The competitiveness of the manager set in the HFRX Equity Hedge universe and Cboe BXM Index has deteriorated over time. Both after GFC and again during 2013 with many institutional and retail funds launching, the pick-up of outright short volatility strategies and short volatility to finance downside puts began en masse. Table 1 and Table 2 clearly show adeterioration as measured by up-down capture post-GFC and post-2013.

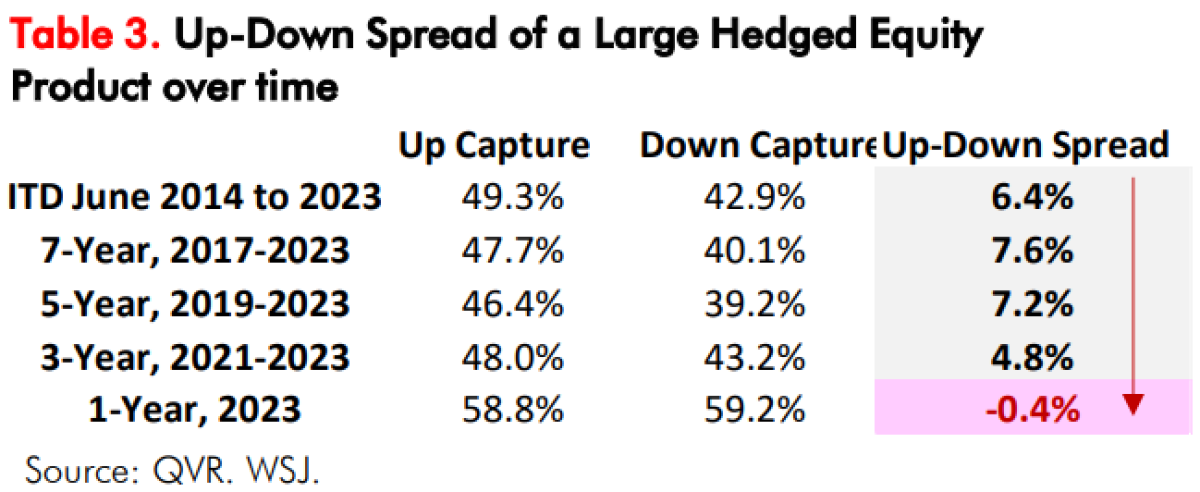

Table 3 shows a large, hedged equity product available to retail investors. This strategy sells an upside call to finance buying a put spread. Effectively, capping upside to pay for ranged downside protection. In the relatively short history, we have seen a slow deterioration of the opportunity set for this strategy as well.

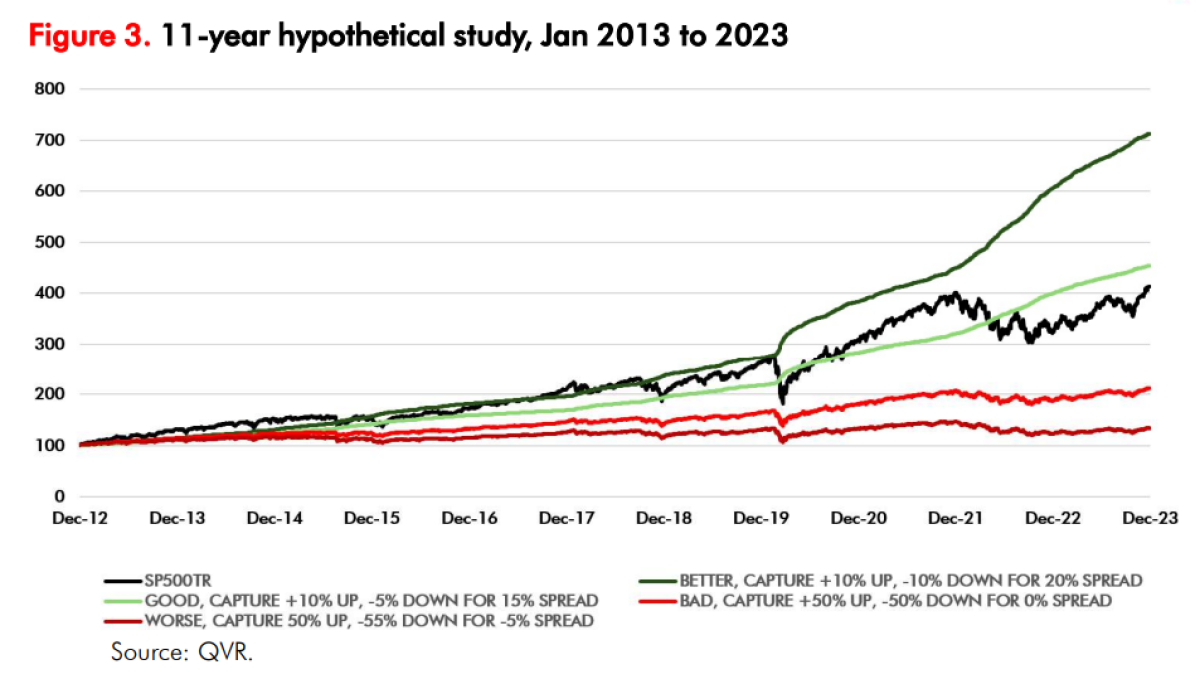

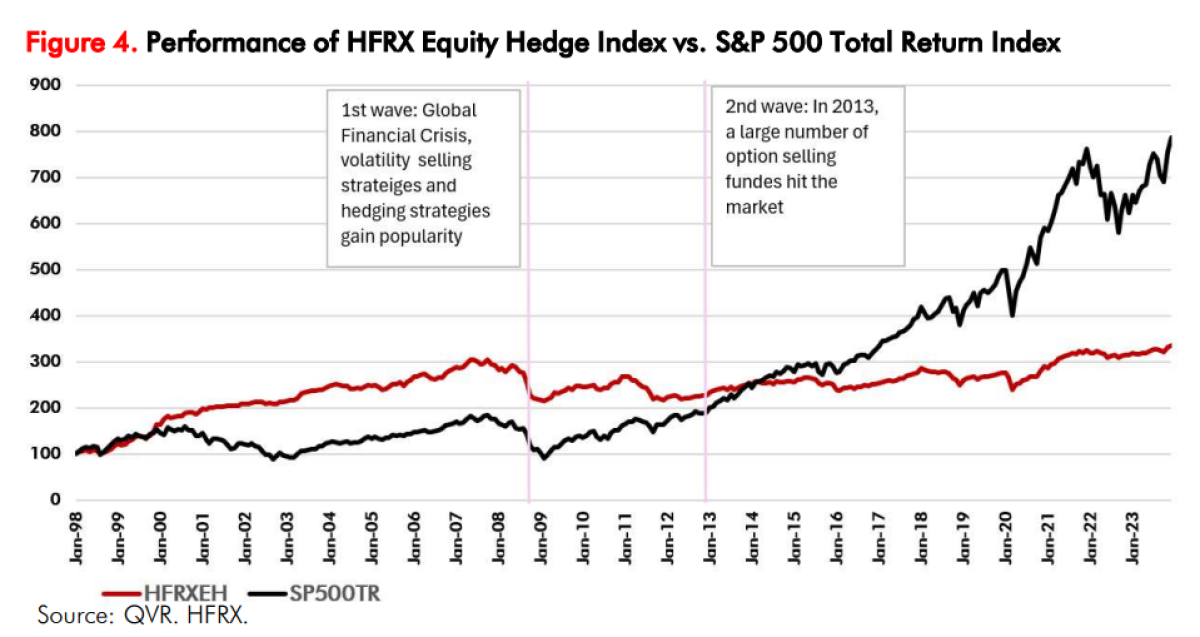

Up-down capture is an important concept to be aware of for derivative strategy returns and hedge fund returns. Historically, a strategy that could provide a +10%, +15% or a very good +20% up-down spread capture would be considered very attractive and had the potential to handsomely outperform the S&P 500 or various benchmarks such as the HFRXEH over time. An up-down capture in the +30% or +40% range would be considered excellent. Many of these same benchmarks are currently on the wrong side, the wrong sign (negative) to be exact. In the below example, we showcase the importance of this over time. Figure 3 shows various up-down capture assumptions on the S&P 500 total return. Figure 4 shows actual returns in a growth of $100 chart for HFRXEH and S&P 500 total return. As discussed, post-GFC volatility strategies and hedging strategies gained in popularity which started to change risk pricing in S&P 500 options. This dynamic picked up again in 2013 with a large number of option selling funds both institutional share class and retail class shares becoming available.

A logical question is, does the average hedge fund now rely on persistent positive equity upside for positive returns?

THIS HAS ARGUABLY BECOME FACT.

Given the deteriorated opportunity set for legacy firms and legacy strategies, we still don’t believe many will course correct. Most are too entrenched in existing programs for their business operations. These approaches are simple and pursued by too many players, degrading returns and impacting implied volatility. This persistent demand for risk mitigating and income strategies has led to a structural shift in risk pricing in S&P 500 options. As a derivatives-based hedge fund manager we are however very happy to live with this relatively new and expanding opportunity set taking a different vantage point.

About the Authors:

Steve Richey is co-CIO, Head of Convexity Alpha at QVR managing the QVR Market Neutral, Hedged Equity and Volatility Hedge strategies. Steve has long career success generating alpha from dislocations in S&P 500 option markets. Steve has spent over 25 years researching and refining S&P 500 trading strategy both professionally and personally. Steve started his trading career at First Quadrant and in his 11 years there, he attained the position of Partner and Director of Trading and Global Options Strategies where he oversaw a $3+ Billion systematic volatility program at its peak. Steve more recently was a PM at Capstone and Parallax. Steve holds a B.Sc. And MBA from Hawaii Pacific University and is a CFA Charterholder.

Scott Maidel joined QVR from Gladius Capital Management where he was most recently a Director of Institutional Solutions. He was previously Senior Portfolio Manager, Equity Derivatives at Russell Investments and Associate Director, Global Trading and Trade Research at First Quadrant. Scott has over 15 years of trading and portfolio management experience with global derivatives.

Scott holds a B.Sc. in Investments and Financial Markets from the University of Southern California, an MBA from Pepperdine University and is a Harvard Business School alumni of the Program for Leadership Development (PLD). Scott is a CFA charter holder and Financial Risk Manager (FRM) certified.